AI? AI! Oh…..

This analysis of the 'AI bubble' was shared with MBMG clients in our monthly update, published on July 2nd

AI Captain?

Robert Recorde was a Welsh polymath of the 16th century, he was a Fellow of All Souls College, Oxford, (his alma mater where he taught mathematics before and after studying medicine at Cambridge). Recorde is best remembered today for creating the equals sign, from two horizontal parallel lines, on the basis that two parallel lines of the same size represented absolute equality. After serving as the Physician Royal, he was appointed as both Controller of the Royal Mint of the Mines and Monies in Ireland. After being sued for defamation by a political enemy, he was arrested for debt and died in the King’s Bench Prison, in Southwark, during the tumultuous reign of Mary I.[1]

AI thinks therefore AI is?

Algebra has been described as the study and manipulation of variables in various fields of mathematics, ultimately using equations (and inequations) as building blocks. The term was coined by Al-Khwarizmi, a 9th century Persian author, from the Arabic al-jabr, meaning ‘reunion’ and used in practice at the time to refer to resetting broken bones.[2] Al-Khwarizmi also coined the terms algorithm and algorism, which evolved into English through Latin usage to represent respectively skilled accounting and arithmetical skill using cyphers (kind of algebraic bookkeeping almost).

“The word algorithm also derives from algorism, a generalization of the meaning to any set of rules specifying a computational procedure.”[3]

This concept of algorithms as a set of rules that specify a computational procedure date back to at Euclid, in the 3rd century BC, and his computation process for computing the greatest common divisor between 2 or more numbers.

Algorithms are the building blocks or ‘backbone’ of computer programming and computer science.[4] By extension, therefore, many of the technological advances of the modern world have been achieved on the back of algorithmic coding that enables large volumes of data to be processed at far higher speed than be achieved through human cognition.

There has long been a sense that delegating the power to initiate decisions to machines is a dangerous subjugation of human authority and humanity’s place as the ultimate apex predator atop the earthly hierarchy. This manifests itself pretty much throughout the recorded history of humanity (influencing philosophy, learning and religious beliefs since ancient times) but has accelerated since the industrial revolution.

Human fears of technology have developed from seeing automation as a threat to their livelihoods, as expressed by the destruction of machinery by Luddites during the Napoleonic wars[5] (although the practice had been around for over 150 years at that stage). By the middle of the 20th century, Isaac Asimov developed his 3 rules of robotics[6] to reassure humanity that the fears expressed in the likes of Fritz Lang's film (and Thea von Harbou's source novel) Metropolis were unfounded.

Fast forward to today’s version of ‘The rise of the machines’.

There’s been a great deal of talk lately of ‘Artificial Intelligence’ as a financial, economic and social game changer.

In our view, much of this talk is at least partially misguided.

AI is a logical and exciting iteration of algorithmic computer science.

However, it is unlikely to manifest as a sea change overnight.

Techno beats?

We are not technology analysts and have no great expertise or special knowledge in the field of IT. That is both a significant limitation and also an advantage in that it grants us a broader perspective.

We understand that technologies have generally emerged and evolved in ways that make terms like ‘industrial revolution’ or ‘technological revolution’ less accurate than if the term ‘evolution’ had been used instead. The effects can be dramatic but can take place over many decades.[7] Often, such changes can give rise to exaggerated fears or expectations, many of which are reflected and dramatized in popular culture. These exaggerated expectations are also often reflected in capital market behaviours. The canal and railway manias of the 18th and 19th centuries exemplified this with expectation-fuelled capital creating unsustainable bubbles as expectations succeeded achievable potential and as technologies were supplanted by later inventions. The building of canals and railways, with the wider benefits that construction conferred on other sector, and the efficiencies and savings that these delivered to the broader economy helped reinforce episodes of rapid economic growth and dramatic returns on investment, both within the manias themselves and more generally. The bursting of the bubbles not only devasted the canal and railway sectors but also created a significant economic drag and a widespread reversal in investment markets.

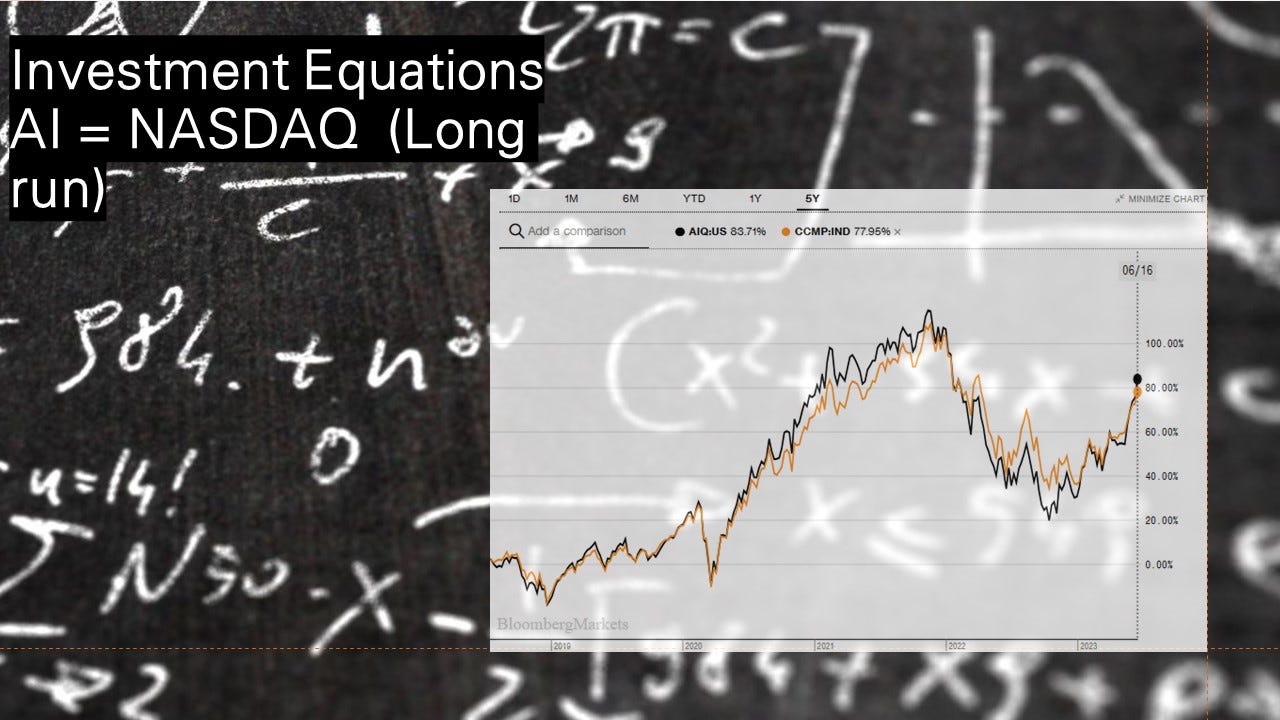

The most obvious recent parallels have included the Tech Wreck NASDAQ crash of the turn of the millennium (when expectations of the revolutionary power of companies related to the internet saw what remained of the NASDAQ fall by over 80% but the majority of companies de-listed and in many cases liquidated or written down to the tiniest fractions of their former values) and the disruptive tech bubble (which saw the Ark Innovation ETF ($ARKK) increase 255% from where it stood 5 years ago to its peak in early 2021 before falling back much lower giving up all those gains and considerably more. The bubble (and the burst) in $ARKK (black line) is clearly apparent in hindsight in comparison to the ‘tech-heavy’ but ultimately diversified NASDAQ Composite Index (orange line) of the last 5 years.

Bubbles and bursts can now happen much quicker and in a much more extreme way.

That said, despite all the recent excitement about AI stocks,[8] AI stocks don’t seem to be in the same territory as the ARKK bubble yet, performing in a broadly similar pattern to the NASDAQ over the last 5 years.

What perhaps isn’t evident from the 5-year chart is the way that AI has outperformed the NASDAQ Index over the last year or so. However, in doing so, it has really tended to match the outperformance of the broader index by the tech sector.

That’s not to say that AI isn’t overvalued in the medium or short term but simply that in the longer term, its overvaluation is inline with the quicker growing broader new economy stocks that make up the NASDAQ and in the shorter term, it is roughly inline with the broad US tech sector.

AI up?

To the extent that AI is a bubble, it’s merely a component of the NASDAQ and tech sector bubbles. Beware of brokers bearing compelling AI stories and understand that the relationship that has driven AI, tech and the NASDAQ so relatively high is mutually reinforcing but we don’t seem to be at the stage yet where there exists an AI bubble fit to burst that will take tech, the NASDAQ and blue chips down with it. It seems more likely to us that all of these would be victims of the same headwinds that will infect and weaken all at the same time, rather than the contagion effects that we witnessed in the Y2K crash.

[1] https://en.wikipedia.org/wiki/Robert_Recorde

[2] https://en.wikipedia.org/wiki/Algebra

[3] https://en.wikipedia.org/wiki/Algorithm

[4] https://www.mycodingplace.com/post/what-is-an-algorithm-and-why-are-they-important

[5] https://en.wikipedia.org/wiki/Luddite

[6] The 3 rules popularised by Asimov (but which he attributed to John Campbell) state that

i) A robot may not injure a human being or, through inaction, allow a human being to come to harm.

ii) A robot must obey orders given it by human beings except where such orders would conflict with the First Law.

iii) A robot must protect its own existence as long as such protection does not conflict with the First or Second Law

[7] Encyclopaedia Brittanica dates the Industrial Revolution as a process spanning the 18th, 19th and 20th centuries - https://www.britannica.com/summary/Industrial-Revolution-Causes-and-Effects

[8] For instance https://www.nasdaq.com/articles/7-top-ai-stocks-to-buy-in-july-2023

MBMG Investment Advisory is licensed by the Securities and Exchange Commission of Thailand as an Investment Advisor under licence number Dor 06-0055-21.

For more information and to speak with our advisors, please contact us at info@mbmg-investment.com or call on +66 2 665 2534.

About the Author:

Paul Gambles is licensed by the SEC as both a Securities Fundamental Investment Analyst and an Investment planner.

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit, it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledge all risks and have been informed that the return may be more or less than the initial sum.