Bittercoin - Putting the crypt in crypto

Why has crypto fallen when stocks have fallen as well?

What’s happening with cryptos?

Crypto token Luna has lost 98% of its value and the digital network of its related ‘stablecoin’ Terra had to be suspended, having fallen over 80%. This came as a shock to many crypto enthusiasts in view of the claims from the crypto ‘industry’ that Bitcoin and other ‘cryptos’ are digital gold, implying a level of security or protection, especially in times of risk asset downturns, in the same way that goldbugs see the precious metal as a diversifier that acts as a kind of investment comfort blanket. .

Like so much of crypto, the claims were never real…..

The problem is that these claims were based on a limited data set and, as has been demonstrated in recent days and weeks, were, like so many unsubstantiated claims about so-called cryptocurrencies, complete nonsense[1]. The idea that cryptocurrencies were a source of protection was just another in an extensive line of spurious justifications for crypto:

First we were told that cryptos were currencies – they’re not. There are empirical explanations readily available that the clearly show that cryptos are not currencies but the simplest way to look at this is that currency is the accepted denomination in a particular jurisdiction – it is issued by the authorities of that jurisdiction who recognise and enforce its validity. Unless a place exists that I’m unaware of called Cryptoland, crypto doesn’t have the minimum characteristics of a currency.

Secondly, we were told that crypto was digital money – it isn’t. Money becomes digital when it is transferred electronically. In different senses, wire transfers, or credit cards or Western Union or PayPal are digital money – electronic transfers that result in or enable transactions. Bitcoin, and other cryptos don’t do that. I recently read that more outlets in America accept Disney Dollars than Bitcoin and that the value of transactions through these outlets is much, much higher in Disney Dollars than cryptos.

Then we were told that crypto was the future of money – however, adoption statistics, like the comparison with Disney Dollars above, show that the future of crypto money isn’t getting any closer.

Then we were told that Bitcoin is a store of value. It isn’t. Self-proclaimed Bitcoin evangelist, Michael Saylor of MicroStrategy explained this in terms of Bitcoin being the “ultimate permanent treasury asset” – effectively a guaranteed store of value in perpetuity. Saylor invested MicroStrategy’s liquid assets in Bitcoin and even borrowed to buy additional Bitcoin, effectively using MicroStrategy as the test case for his claims. At the time of writing, the value of MicroStrategy Inc. has fallen by over 80% in the last 6 months.

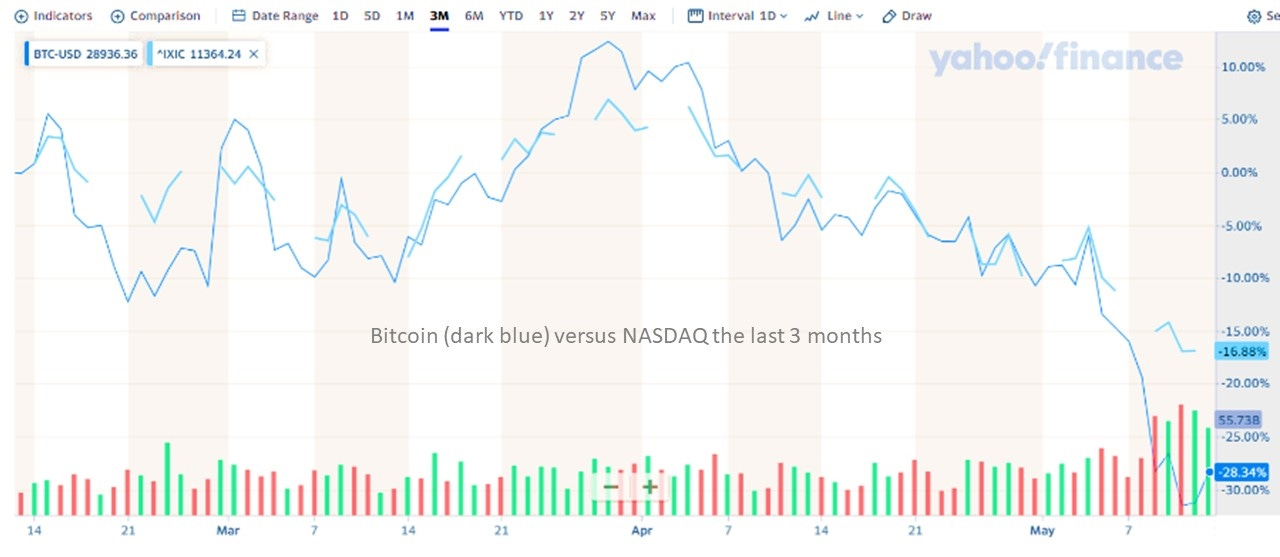

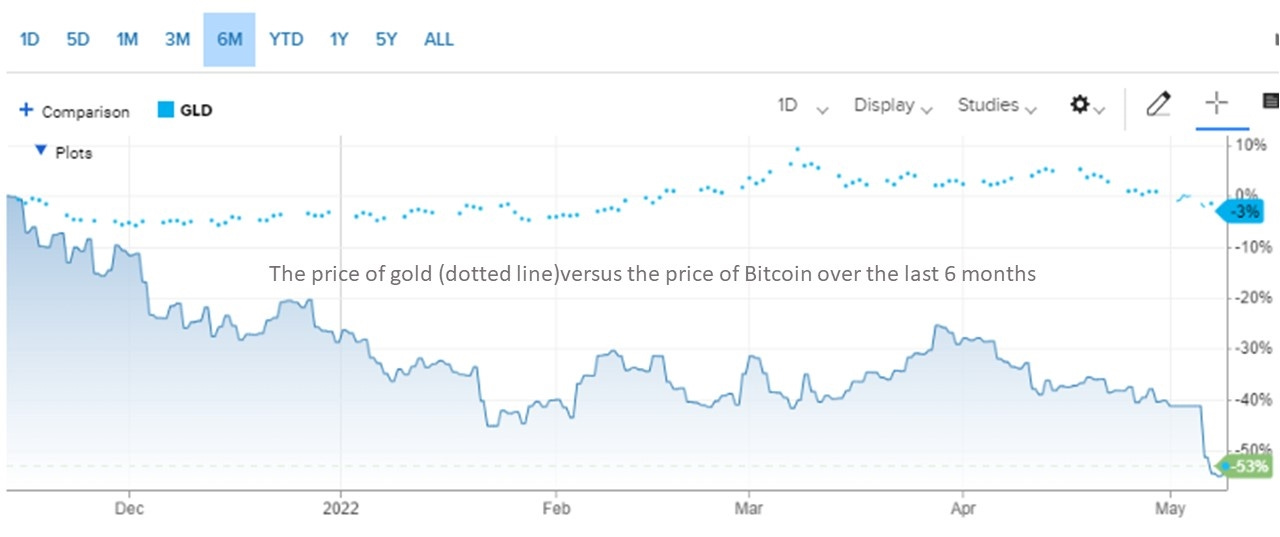

The store of value argument is similar to the digital gold claims, It had in fact been refuted in the first quarter of 2020 when stocks crashed, and gold rallied[2]. Bitcoin followed stocks down with a correlation of 0.8 (i.e., it moved in the same direction as the imploding equity markets around 80% of the time). It’s correlation to gold was less than 0.1 (i.e., gold and Bitcoin moved together less than 10% of the time).

All that’s Bitter is not gold

What does that mean?

In other words, we’ve known for some time that when stocks crash, like in March 2020, cryptos tend to move in the same direction and to a greater extent (i.e., when stocks fall, cryptos fall more). There are a number of explanations for this:

The stock price rallies following the GFC and following the COVID lockdowns were, to varying degrees at various times, fuelled by liquidity – i.e., the inflow of new funding into asset markets. This drove many assets to higher prices but especially those, such as illiquid or closely held assets, which respond most to liquidity. Liquidity, as we’ve remarked before[3], seeks out the situations where it will have the greatest impact.

This can be seen in the most egregious beneficiaries of liquidity-fuelled price ramps, from the ARK series of Exchange Traded Funds to the various meme stocks.[4] But it is most evident in crypto. Crypto’s pricing mechanism is almost uniquely sensitive to liquidity. Crypto has no inherent value. Its price is determined by what buyers are willing to pay and sellers are willing to accept based entirely on their subjective valuation.

How does that work?

Bitcoin fans try to claim that this is the same as an asset, financial or otherwise. However, that’s another misrepresentation.

Assets have a value – businesses have expectations of the cashflow that they will generate, properties have a replacement cost to build, commodities have a value based on their usage. The price that the market pays may well also reflect a premium or discount that the market subjectively applies but this is only a component, usually the much smaller part of the asset’s pricing. With crypto, there is no such embedded value. The only component of pricing is the subjective premium.

What makes this worse is that the premium is subject to manipulation. If I want to sell stocks, I have to go through an online or physical exchange, where, generally, the transaction is visible, transparent and the price set by willing and genuine participants. Crypto enthusiasts (or hodlers as they like to refer to themselves, rejoicing in their own illiteracy as a badge of honour) can simply drive-up pricing by selling from themselves to themselves at prices that aren’t grounded in reality (i.e., money doesn’t change hands between different parties, so the price is really just a work of fiction, it doesn’t represent anything other than meaningless keystrokes).

This means that other than where reality intervenes, the price of Bitcoin can drift up to infinity without being anything other than a multilevel, multiplayer videogame. However, these patterns attract liquid capital, which on some levels can’t distinguish between Bitcoin pricing and a genuine bid and offer auction. These real inflows serve to drive prices higher as real bidders now join the manipulators and real sellers replace the falsified sellers. In an upwards market, this simply serves to drive Bitcoin prices inexorably higher. If liquidity dries up across all markets, then genuine financial assets might stop increasing in price or even dip slightly. If inflows into cryptos cease, then the game of fantasy bid and offering resumes and the prices continue to increase, albeit at a slower rate. This gives the lie to the claims of being uncorrelated.

However, when major outflows occur, then financial markets crash, like in the first quarter of 2020 or like this year so far. When that happens, the overwhelming activity in crypto markets becomes the selling of real sellers. Fake bids can do little to mitigate this when it becomes overwhelming – if a genuine seller wants to sell his Bitcoin and the best real bid that he can get is $25,000 per coin, crypto exchanges can’t facilitate fake transactions at a higher price. Off market (what are know as cold wallet) transactions can continue to happen at any price but look ridiculous if they don’t closely track what’s happening in real transactions.

Conclusion

By design, Bitcoin will appreciate in price without any genuine transactions needing to take place.

When there are buyers, this exaggerates the uptrend.

When there are a flood of sellers, looking to unload cryptos with a fundamental value of zero, which is what happens in conditions that also drive equity markets lower, then cryptos freefall, with little help from the fake pricing process.

Cryptos tend to fall more sharply because their pricing is entirely a premium over the actual value per coin of $0.00 and therefore there is much less of a floor than with assets that have fundamental value.

The whole crypto system is built on the assumption that the manipulated liquidity-driven pricing is valid. Therefore, derivative features of the system like stablecoins (a method to convert from crypto to real money) also come under pressure, because their own pricing is based on the manipulated bubble premium of the crypto system, while their own inherent value is a derivative of zero. Stablecoins like Terra have had to halt trading, having lost over 80% of their value (remember, these are so called stablecoins, their value is meant to be er stable) because their linked assets like the coin Luna have lost over 98% of their value (and yet being worth zero, paradoxically their price is still comprised 100% of ‘premium’, they remain fundamentally 100% overpriced, just as they were when they were 50 times higher in price).

Crypto and stocks have fallen at the same time and always will until or unless the crypto system is changed or banned. We don’t know whether that will happen at this time. If it doesn’t, then if and when the outflows stop, the previous game of price manipulation through fake transactions will lead prices back higher again.

Numerous studies have revealed, at various times, that the amount of ‘spoof’ or fake trading in Bitcoin is 95% or more.[5]

[1] https://www.morningstar.com/articles/1088689/is-cryptocurrency-really-a-portfolio-diversifier

[2] https://themarket.ch/meinung/the-myth-of-the-uncorrelated-crypto-investments-ld.1686 In fact, this myth had been exposed even earlier https://www.ft.com/content/3496b6ff-cc2f-443c-9a25-67ff751f5589

[3] https://mbmg-group.com/article/dilemma-between-liquidity-fueled-bubbles

[4] https://mbmg-group.com/article/hot-stocks-cooling-down

[5] Ninety-five percent according to Bitwise https://www.cnbc.com/2019/03/22/majority-of-bitcoin-trading-is-a-hoax-new-study-finds.html