Everything ventured? The inevitable fall of Silicon Valley Bank (& others)

The valley of the shadow of death

The Santa Clara Valley in Northern California, better known for the last half century as Silicon Valley is home to many leading global technology companies (including the HQs of 30 of the world’s leading hi tech multinationals) along with incubators and accelerators housing thousands of start-ups or early-stage ventures.

From Heart’s Delight to Silicon Valley

Until the late 1960s the region had been known as "the Valley of Heart’s Delight” being the world’s largest fruit-producing and packing region. However, the region had already built a focus on science and engineering partly through its role in military technology R&D, from researching and developing key technologies, first for the US Navy, subsequently for the Pentagon[1] and latterly for NASA’s Ames Research Center. Another factor was the involvement and financial and academic support of Stanford University. Stanford was seen as a key standard bearer in California’s focus on forging its own identity as a bulwark against the threat of exploitation by predatory capital from the east coast, especially an ascendant Wall Street. Stanford forged a strong identity in engineering, encouraging the foundation of businesses such as Hewlett-Packard[2], Eastman Kodak, General Electric and Lockheed in what was later to become Silicon Valley.

Venture Scouts

VC in post-war America developed in a uniquely American way, largely because what in Europe was designated ‘merchant banking’, namely sourcing and intermediating loans and capital from investors to businesses, was prohibited to retail, deposit-taking banks, since the introduction of the US Banking Act of 1933.[3]

The gap was filled on the east coast by pre-war investors such as E.M. Warburg & Co., J.H. Whitney & Company and the family offices of America’s most successful business families of the 19th and first half of the 20th centuries. These were also joined by ‘newer money’ and also by the war chests of the Ivy League and other elite east coast universities. Harvard and MIT were significant drivers of one of the earliest successful post-war VC houses, ARDC.

In California, following the tradition established by Stanford in providing locally fund to nascent Silicon Valley tech enterprises in order to prevent reliance on the dominion of Wall Street capital, the growth of the technology eco-system attracted and was partly driven by a new wave of venture capital, raised by financiers operating in Silicon Valley.

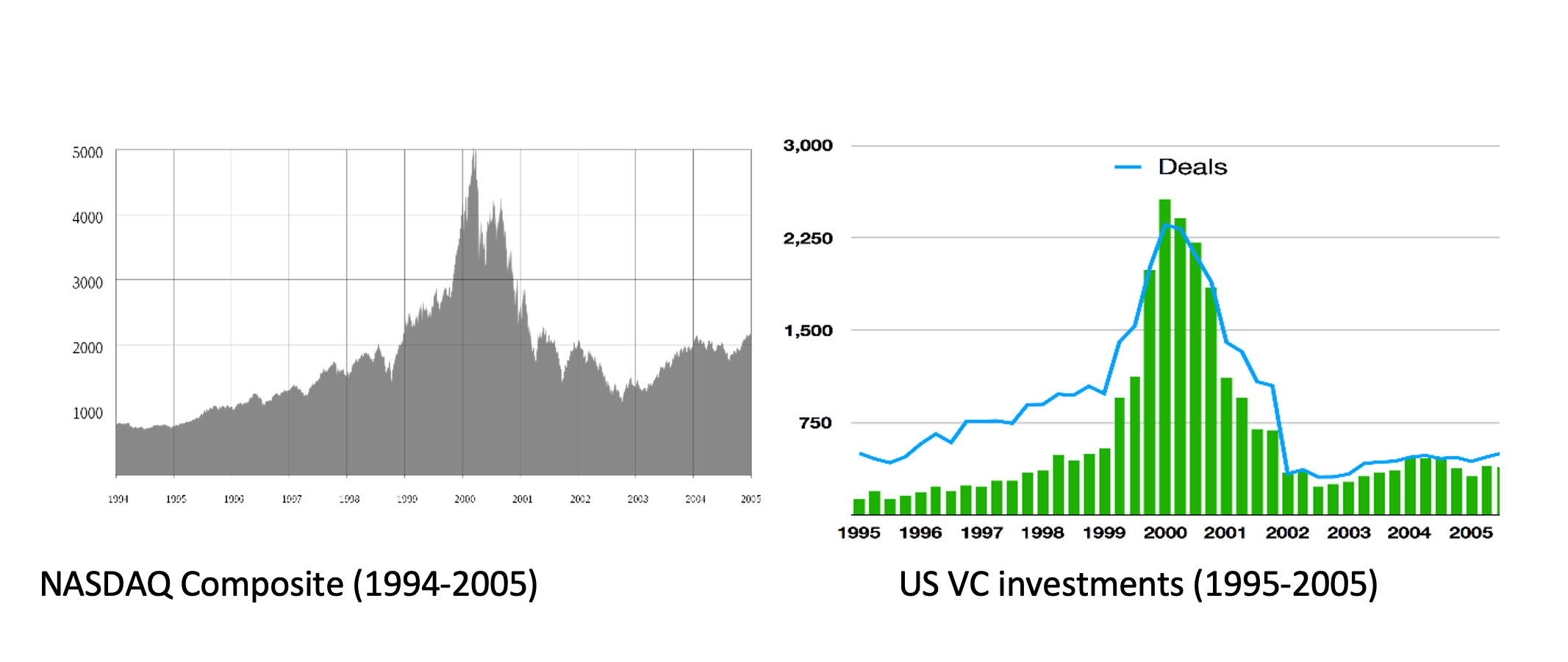

One of the earliest operators in Silicon valley was Kleiner Perkins Caufield & Byers,[4] who, in 1972 set up office on Sand Hill Road (SHR), a quiet suburban route that terminated in the Stanford Shopping Center car park. The over 900 ventures backed by KPCB include AOL, Amazon, Compaq, Google and Twitter. Sand Hill Road has become known as New Wall Street and now houses over 50 other major VC firms and also competes with Manhattan to offer the most expensive office space. SHR also became the epicentre of the Dot-com bubble of the late 1990s, which saw thousands of companies publicly list, primarily on the NASDAQ, in a relatively short period, before, in most cases, failing and delisting. Despite this, Silicon valley accounts for over 1/3 of US VC investment.

New Model Harmy

The Tech-wreck of 2000-2002, which saw the NASDAQ fall by 78% from peak to trough followed the 400% run up in the index in the preceding 5 years. This correlated with VC funding activities:

Following the tech-wreck and the antipathy towards the egregious monetisation by VCs, the prior model of building business narratives, prematurely listing unsustainable models on public indices at unrealistic valuations and then squeezing as much price, but not value, from them to reward VC investors was no longer viable. The model was tweaked, partly out of necessity, but partly in response to the post 2008 ZERO Interest Rate Policy (ZIRP) environment, which made viable any business that could raise enough funding to pay its operating expenses. Instead of the now frowned upon practice of listing in order to then manipulate higher public valuations of stocks with limited free floats, the new trick became to manipulate the values to nosebleed valuations of the private companies before they listed. With private companies, this could be achieved away from the prying eyes of once bitten twice shy investors and market regulators. An unregulated private bubble, primarily driven by VC interests and their poster boy, Masayoshi Son of SoftBank, was able to run uninhibited to nosebleed levels, without the significant risk that it posed being obvious. VC is always somewhat speculative in that you’re buying into future assumptions of execution with far less solid justification and precedent than with established businesses. This can make it a leap of faith, although of well-run at least it can be an informed leap of faith. However since the era of disruptive tech, these are completely groundless assumptions – a bit like playing fantasy football but with real money. To make this blind leap even more divorced from reality valuations have manipulated techniques that in public markets would be illegal but in some private markets have become Standard Operating Practice. As we’ve been saying for some time ‘mind the ever-widening gap’. These various VC machinations have been excellently tracked by Matt Levine in his Bloomberg column Money Stuff, although myself and the team have also warned about these issues:-

“the next bubble that’s going to burst….price discovery on a unique private asset that nobody knows if it will ever turn a profit is impossible…pure financialization…this isn’t just SoftBank, this is a whole industry that’s now grown up doing these pure accounting exercises to create fantasy value…whatever you do, don’t take your private equity money to California…they’re just some financial monster”.[5]

In our April 2022 outlook we noted –

For the last few years, we’ve talked of the scourge of VC and its poster child Softbank.

Our concern is that the whole unicorn phenomenon is a repeat of the dotcom nonsense of over 20 years ago, where asset prices of Potemkin businesses are ramped to such ridiculous levels that investors are writing cheques that the companies can never fulfil.

BSBS (BullShit Balance Sheets) redux

This echoes the events that led to the dotcom bust, tech-wreck and NASDAQ crash at the start of this millennium.”

Is History Repeating? Softbank Share Price 2000-2022

We asked if implausible VC valuations were a bed of nitro-glycerine (to borrow Bill Gross’ iconic phrase) atop which resided the likes of ARK and noted that following the Dotcom bust, the NAV of Cathie Wood’s Tupelo CM Fund fell by well over -80% before it was shuttered:.

Is The ARKK More Like The Titanic

We observed that “The consequences of such a repeat meltdown are highly explosive as well. Contagion would move from VC, through Tech to Growth, ultimately rendering all risk assets potentially vulnerable”

Do the broader indices have some catching up, or rather catching down still to do?

Similar questions apply following the recent failure of crypto facilitator bank Silvergate and last Friday’s closure of Silicon Valley Bank.

First SBF and now SVB?

One popular manipulation In a ZIRP environment that has been highlighted by Levine has been the use of extreme follow-on investments. In an environment where time value of money was expunged, it suited VCs to make unnecessary additional cash injections into companies they had already invested in.

Potentially this had the effect of:

Increasing the VC stake by diluting, founders, sweat equity employees, early-stage funds (families and friends);

Extending the life span of otherwise non-viable businesses – income is unnecessary if your cash inflows from investment can cover all your outgoings;

Improving financial metrics in the eyes of the world, holding enough cash to cover your burn rate almost as far as eyes can see into the future.

In reality, even without higher interest rates, this model would have eventually foundered on the rock of the real world. Increasing rates above zero simply brought this day of reckoning sharply forwards. In 2019, when we issued the warning that VC would be the next bubble to burst, the Fed had started on a journey to tightening. Only the intervention of the pandemic forcing the Fed to perform an about turn (and some!) delayed this by a couple of years. The intersection between VC and the world of crypto (often disguised as FinTech or DeFi) amplified the eventual scale of reckoning.

Fast forward to 2023 and VC-funded firms with significant cash balances have largely parked these with crypto/VC-friendly banks such as Silvergate, SVB and, announced yesterday, Signature Bank. The deposits that these banks held as liabilities comprised real values that have to be paid out on demand. The assets that they held were a mix of real assets that were marked down because of higher interest rates (e.g. US Treasuries) and loans to and other assets built on the VC’s excessively ramped ecosystem, many of which will never be repaid. The reality of cash value deposits being called when SVB was unable to persuade investors or lenders to extend funding based on its BSBS, resulted in the cash crunch that has seen SVB and Signature taken over by regulators in the last few days.

It’s too late to ask whether there will be contagion. The contagion actually preceded SVB’s collapse – this is just one in a chain of events that interact, rather than a trigger event in itself that has come out of nowhere;

the collapse of the narrative of crypto has coloured overhyped related disruptive fantasy businesses, this drives down other disruptive tech VC sectors

this then starts to drive down all disruptive tech VC valuations

this then feeds through to listed disruptive tech (Uber, Lyft, AirBnB etc)

this then starts to feed through to secondary sectors (e.g. SVB)

it also hits the balance sheets of major holders of inflated assets (GOOG, AAPL, FB etc) and ultimately Softbank, MicroStrategy .

This could sour sentiment across stock indices.

Other banks could be affected.

There could be a wave of tech bankruptcies.

We know that many major banks have provided facilities via e.g. Vision Fund but the known/expected write off numbers are small enough to be a bad quarterly earnings report for major banks.

However, based on what we know none of this contagion necessarily represents a systemic threat. Contagion generally becomes systemic once it involves large scale exposure to borrowing. In terms of scale, the entire US VC industry is less than half a trillion Dollars. The real estate market, whose correction brought about the 2007-9 crisis in America is over 120 times larger and is predicated on loans made by tens of millions of Americans. The VC borrowing that will inevitably written off is a relatively small part of the industry – by definition it seeks Venture Capital because of the restrictions in gaining access to traditional bank and other funding. Based on what we know, crypto winter could become VC winter which could deepen the sense of tech as a frozen wasteland and see equity markets cool but without the same debt default consequences that the US economy experienced 15 years ago, there is no reason to fear that this will become systemic.

However, if the borrowed money losses (like in the tech wreck) are more significant than we think, that’s when we might need to re-evaluate the possibility of systemic risk. If somehow the tentacles go further, then it could be a bigger problem than we currently realise, and maybe there could be a Lehman moment, when it was suddenly apparent that the losses of 3 BNP esoteric credit funds and 2 Bear Stearns Funds had been a systemic early warning sign.

[1] One of the most heralded interactions with the Pentagon was the creation and operation of ARPANET, the precursor of the internet.

[2] The garage in which Stanford graduates Bill Hewlett and David Packard developed audio oscillators in 1938 became known as the ‘Birthplace of Silicon Valley’. The business that they founded later became one of the earliest tenants in what was to become Stanford Research Park and were among the earliest recipients of VC funding from Stanford. A few years after H-P took up this tenancy, Bill Shockley (inventor with 2 colleagues of the first working transistor) , following a disagreement with his employer, left his job with Bell Labs in New Jersey to Palo Alto to care for his elderly, sick mother. Shockley pioneered the use of silicon in transistor manufacture. Spin offs from Shockley’s firm (which happened frequently due to his acrimonious management style) included Intel. The resultant primacy of silicon-based transistor manufacturing led to the coining of the term ‘Silicon Valley’ by Don Hoefler, a journalist for Electronic News. By the 1980s, the term had gained widespread traction, becoming a euphemism for the American technology sector, at the time that the ‘Homebrew Computer Club, founded by Fred Moore(of the eponymous ‘law’) and Gordon French, was attracting alumni including Jobs and Wozniak. The club has been credited with having gestated Microsoft and Apple.

[3] The Act is best known for the four provisions contained within it that separated commercial/retail and investment banking. These provisions are generally referred to by the names of the legislative sponsors, Carter Glass and Henry Steagall, as the Glass-Steagall Act.

[4] Sequoia capital also set up in 1972, although arguably were slightly slower out of the blocks although made up lost ground by being a major early backer of Apple Inc, which enjoyed a $1.3 billion listing in 1980.

[5] https://www.asianinvestor.net/article/unicorn-valuations-are-fit-to-burst-warn-investors/454833