Stimulus – Will it Work?

by Paul Gambles & James Fraser on 02/02/2021

The following Flash introduces the Feb Outlook which is available on request – please send an email to info@mbmg-investment.com

The latest US stimulus dive worth USD 1.9 trillion will either be successful or it won’t be. If successful (which is the less likely option in our view but we’re not ruling it out) then that should signal a possible end to stimulus or at least reduction in terms of its scope and scale. This would signal stability, higher growth, a sustained rebound in US interest rates and should push USD higher versus most other currencies, and potentially place US treasuries on a bear-market path for several months (although we could also see a situation where almost all asset classes rise due to the excessive liquidity that will have been created).

Even before Covid-19 appeared, the Trump administration’s 2018 USD 3 trillion package wasn’t able to provide a sustainable growth or rises in interest rates and by July 2019 the Fed began to reduce its benchmark target rate range for the first time since the Global Financial Crisis and by October that year implemented its third cut, each of 0.25% in the space of four months, reducing the target range to 1.5% - 1.75%. The Fed highlighted the possible shocks of a trade-war with China but really, there just hadn’t been any improvement in the first place and most of the financial windfalls from the corporate tax cuts had been used by the large public companies to buy-back shares while others seemed to simply save it rather than investing in business expansion. Today, the Fed target rate stands at a target of between 0.01 - 0.25%, a similar range to post Global Financial Crisis. While the Fed was on a steady path to raise rates in 2018 it spent a good deal of time fathoming out why there was no sign at all of inflation or significant impact on average payrolls - low skilled work dominated the new non-farm payrolls and still do.

If implementation of the latest USD 1.9 trillion package which began last week with the distribution of USD 600 handouts to most Americans, follows the same path, then that could signal somewhat of a contraction and possibly crisis ahead or, at the very least, a risk-off episode, which should more than likely also cause the USD to strengthen against most other currencies. So, in addition to our views below, our conclusion is also a higher expectation for USD to strengthen.

Our overview remains

1. The outlook remains both unclear and fragile;

2. Asset prices don’t seem to be pricing this in;

3. Asset prices are reflecting certain policy expectations that, to us, seem highly unrealistic

One difficulty is reading longer trends when faced with the disruption that occurred last year. It remains our view that many participants are taking the rebound from last year’s lows as signs of recovery, when we all know that if dead cats are dropped from a great enough height will bounce quite high (note: no cats were harmed in the writing of this flash note).

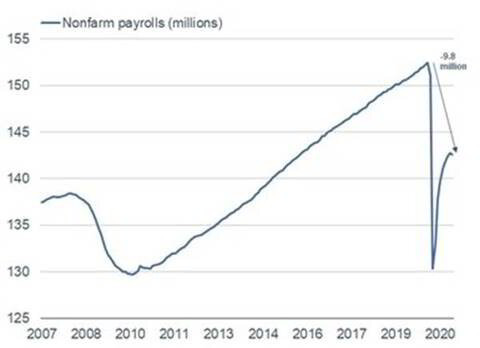

Non-Farm Payrolls rebounded to late 2015 levels and now show signs of weakness

There are still around 10 million less American employed than there were and around 12 million less than there would have been had the pre-Covid-19 employment trend continued.

Source: FRED

A marginalized US economy caps potential

That feeds into all kinds of secondary effects including that a Marginalized Society will limit the opportunity for a post-Covid-19 rebound. Downward wage pressures on the lowest paid (December’s total US job losses netted 100% to women and over 100% to black women – i.e. Women account for 100% of jobs lost in December, new analysis (cnbc.com)

Money Supply ebbing but, so far, it isn’t taking TESLA or FANGS with it

The engine that powers the US economy has stalled, having received a huge boost from stimulus in March/April last year (around $2.5 trillion) which, as expected, slowly dissipated in order to find a base. The fall-off in 2021 could be a blip, things could pick up, but this is the biggest direct contributory factor behind the poor employment and wages data. America Inc. has been contracting or at least its rate of expansion has been falling sharply towards zero, for around a month now and this needs to be watched very closely. Yes, vaccines and stimuli and good ol’ American never say die might turn this round – but another few weeks of this would be a major worry.

With the latest stimulus a make-or-break indicator, there still is an opportunity to accumulate long dated treasuries and underperforming but commercially resilient S&P 500 sector – the high dividend, low volatility index.

MBMG Investment Advisory is licensed by the Securities and Exchange Commission of Thailand as an Investment Advisor under licence number Dor 06-0055-21.

For more information and to speak with our advisor, please contact us at info@mbmg-investment.com or call on +66 2 665 2534.

About the Author:

Paul Gambles is licensed by the SEC as both a Securities Fundamental Investment Analyst and an Investment Planner.

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit, it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledge all risks and have been informed that the return may be more or less than the initial sum