MBMG Flash - Steering between the horns

Rising Volatility and the Addiction to 'Public Debt'

Portrait of a black cow (with horn protectors) in Norway- Ernst Vikne

MBMG Investment Advisory

Asset allocation is always challenging. In hindsight, while the last 12 months have been no exception, at least the correlations between different asset classes and sectors have been reasonably orderly. In the chart below, we can see that other than the stark outperformance of value stocks in late February/early March and the subsequent reversal in that, correlation between all the factors (i.e. the characteristics of different stocks, such as value, growth, momentum and quality) has been tight:-

The black line represents growth; orange is value; red, momentum and blue, high quality.

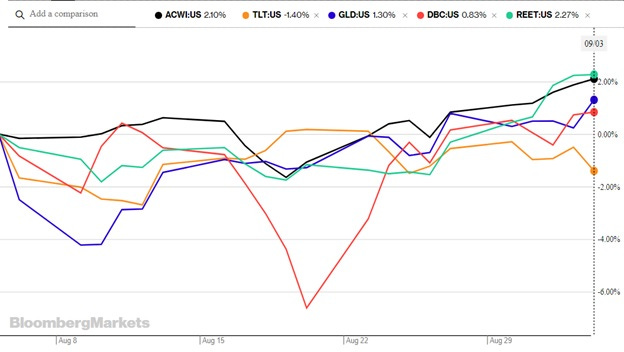

But… Last Month, A Dramatic Rise in Volatility Between Risk Asset Classes Emerged….

The volatility of each asset class and the cross volatility between asset classes has increased perceptibly:

One reason for the orderly nature of growth and momentum stocks is that these have been driven up by relatively few heavy-weight stocks while value, which can be broader-based, involving rather more companies, typically lags their performance. If this continues then could be a relatively benign shift to a new normalization, in which hot stocks and hot sectors lead the markets even higher. Alternatively, it could be something more sinister. We are, in the words of the Fed, 'data dependent' and steering between the horns with a balanced mix of funds and ETFs from a broad array of asset classes would, so far at least, have enabled gains on growth and momentum to easily cover losses in defensive hedging assets such as US treasuries.

Long-term Yields and No Convincing Break-out

The most reliable longer-term return indicator remains long-term inflation (and therefore growth) expectations. While long US treasury yields have deviated far more than is typical in the last year or two, the price action suggests that the long-term downward trend looks like it remains in place:

Money Creation

The rebound in long duration US treasury yields during the Q1 this year (this means lower bond values), following the collapse in yields in 1H last year (higher bond prices) only took us back to the approximate levels of the 30-year US treasury market at the start of the pandemic.

If yields had gone higher (bond prices lower), we might have started to become more concerned of a cyclical bear market emerging in these treasuries but that really would have required 30-year yields pushing 4% before continuing their downtrend. Contrary to inflation bulls’ predictions, there is no obvious bear market.

Convoluted Logic Highlights Stimulus Need

Higher inflation announcements this year have at times actually supported bond prices (when they might normally be expected to harm them) because of the contrived logic that removal of stimulus (to tame inflation) would hurt growth and asset prices and lead to a more aggressive resumption of stimulus going forwards. This logic is convoluted, fragile and at least partially ill-founded but it likely does reflect an underlying lack of confidence in an economy without stimulus.

The creation of ‘money’ remains the biggest single input into economic activity. Prior to the pandemic, this predominantly reflected credit creation by banks. However, one paradigm shift that remains largely misunderstood is how the direction of economic growth and capital market price direction has largely shifted to reliance on government money creation, reflected in the quite inappropriately named ‘Public Debt’.

For further detailed discussion and analysis please review our Autumn Outlook available upon request at info@mbmg-investment.com.

MBMG Investment Advisory is licensed by the Securities and Exchange Commission of Thailand as an Investment Advisor under licence number Dor 06-0055-21.

For more information and to speak with our advisor, please contact us at info@mbmg-investment.com or call on +66 2 665 2534.

About the Author:

Paul Gambles is licensed by the SEC as both a Securities Fundamental Investment Analyst and an Investment Planner.

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit, it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledge all risks and have been informed that the return may be more or less than the initial sum.

Copyright © 2021 MBMG Group, All rights reserved.

You are receiving this email because you are a client and subscriber of MBMG Group.

MBMG Group | 75/56 Ocean Tower2, 26th Fl., Soi Sukhumvit 19(Wattana),

Klongtoey Nua, Wattana, Bangkok 10110 Thailand