Paul Gambles and IA Team

Contagion – ‘it goes where it can impact the most and leaves behind that which it cannot’.

Capital always does what capital does. It flows to the places that make the highest returns and the highest returns over the last year were some pretty crazy places. As we know it was Tesla, Ark funds, cryptos and SPACs (so-called ‘blank cheque’ special purpose vehicles where well-known managers raise funds from investors, and then find venture capital and private equity opportunities to invest into and to list on markets in reverse listings and public offerings).. That's just where the best market returns have been. That's a fact of how liquidity fuels bubbles but it doesn’t last forever and the liquidity that's driven these bubbles is not coming in at the same rate anymore so we could see these bubbles heading into a pretty nasty storm. Remember, liquidity-fuelled, bubbles need continued increasing inflows and we're not getting that anymore.

In short, liquidity has fuelled risk assets, especially meretricious[1] ones, but value is difficult to discover in risk assets, except where it reflects discounts in other asset classes such as gold bullion, that hasn’t attracted bubble capital.

Liquidity has largely Ignored Higher Quality, less Volatile assets.

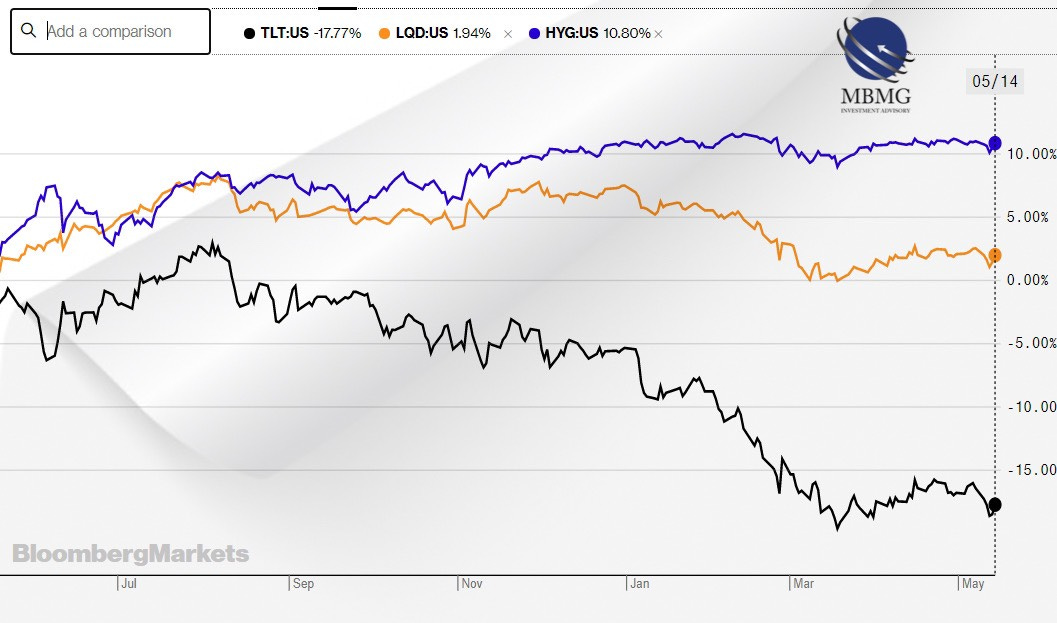

Another example of an underperforming asset class is US treasuries. In a mirror image of the equity market, high risk, illiquid corporate bonds have dramatically outperformed both less risky and less illiquid high quality corporate bonds and highest quality, most liquid treasuries:

[1]Meretricious. (noun) apparently attractive but having in reality no value or integrity- OED

This during a period when deteriorating economic conditions led to record number of credit downgrades (which should have adversely affected high yield above all).

Just to recap- liquidity, logically, found its way to the places where it had the greatest impact but, if anything, this led to outflows from the places where it would have the least impact, such as gold and treasuries (physical gold and gold miners have rebounded in recent weeks but mainly for the wrong reason which seems to be ‘mispriced’ inflation expectations).

Exaggerated & Misplaced Inflation Expectations Higher inflation expectations over a short-term are justified as of course many commodities are higher than they were a year ago when the price of oil, for instance, traded at a negative number as well supply chain disruptions and post-Covid lockdown bottlenecks. Several other commodities including lumber, rubber, and steel have also spiralled over the past 12months (along with e. g. freight and transport costs for equivalent reasons) but that doesn’t equal inflation because these prices are supply shocks and are not ‘sticky’ and the mechanisms of these markets will work them out before too long, and in fact this seems to have started already. Sticky factors, like wages, still seems suppressed in real terms.

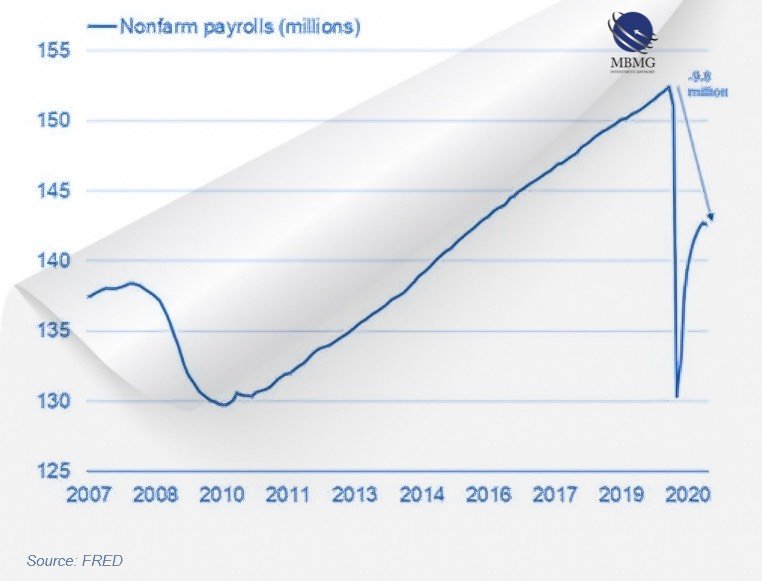

Stimulus hasn’t adequately addressed needs of the Job Market The number of US employees remains almost 10 million below pre-COVID levels and the best part of 14 million people less than it would have otherwise been projected to be at this stage:

Debt, Demographics and Dispersion reduce the effectiveness of US Stimulus of US employment (and real personal income) which was stagnating before the COVID outbreak. Growth has been in a secular decline for multiple years, private debt levels remain at post-GFC highs and long-term growth expectation indicators remain bleak. On top of these structural issues, debt level and dispersion worsened during the COVID lockdown and COVID ‘scarring’ effects are an added psychological burden on re-opening. The economic outlook was challenging before COVID. The failure of stimulus to address or adequately mitigate these challenges has only made this outlook even darker. Unless there is a radical change in the nature of stimulus policies, there is no reason to expect that additional stimulus measures will have any impact other than fuelling further liquidity bubbles in other risk assets, while doing nothing nearly enough to address the economic challenges.

Further Stimulus will likely create new Bubbles The real economy is an even less attractive proposition for generating immediate returns on capital and therefore, along with low risk, liquid assets, appears to have also failed to benefit. Capex and hiring remain extremely subdued (we’ve covered this in pieces such as The value of US 20 year treasuries has fallen by over 11% this year ...Should we all be buying treasury bonds? (mbmg-group.com) and Stimulus – Will it Work? (mbmg-group.com).

This note is based on excerpts from our MBMG May/June 2021 Outlook. To receive your Outlook please contact MBMG Investment Advisory at info@mbmg-investment.com.

MBMG Investment Advisory is licensed by the Securities and Exchange Commission of Thailand as an Investment Advisor under licence number Dor 06-0055-21.

For more information and to speak with our advisor, please contact us at info@mbmg-investment.com or call on +66 2 665 2534.

About the Author:

Paul Gambles is licensed by the SEC as both a Securities Fundamental Investment Analyst and an Investment Planner.

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit, it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledge all risks and have been informed that the return may be more or less than the initial sum.

Interviews with Paul

CNBC Asia: 8 Jun 2021 at 07:10 am BKK time

More to follow ............stay tuned

Copyright © 2021 MBMG Group, All rights reserved.

Our mailing address is:

MBMG Group | 75/56 Ocean Tower2, 26th Fl., Soi Sukhumvit 19(Wattana),

Klongtoey Nua, Wattana, Bangkok 10110 Thailand