MBMG IA Flash - Higher short-term rates today creating a worse long-term outlook

That's What US Treasuries are telling us!

Paul Gambles and IA Team

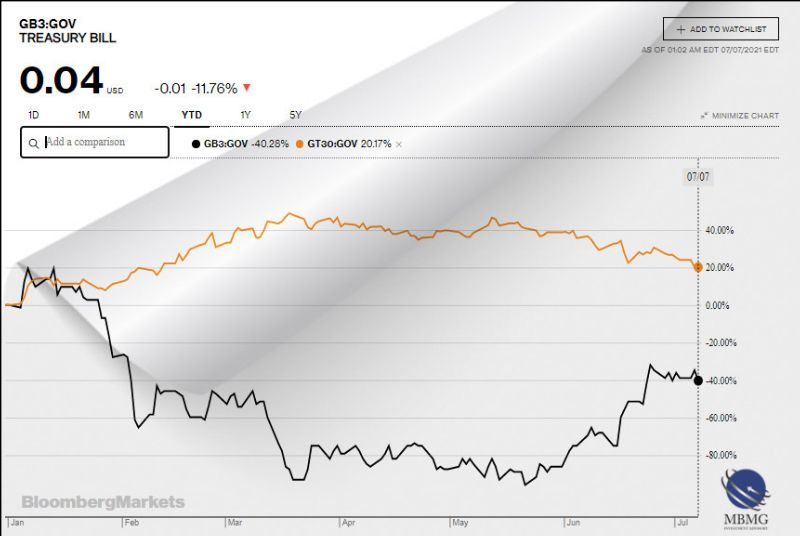

Recent (loose) talk by the Federal Reserve’s Open Market Committee (which, at least in its own ‘mind’ dictates American monetary policy, such as setting notional short term interest rates) about tapering the amount of assets that it buys every month or other forms of monetary tightening (basically making borrowing more expensive and/or less available) saw short term interest rates move higher while at the same time longer term treasury bond interest rates (20 years or more) have fallen sharply - in other words, the extreme ends of the treasury curve, short term and long term, have moved in different directions which is significant in that it typically indicates the future outlook for economic conditions such as growth and inflation.

What changed last month was that short term rates, which had fallen since late January, began moving higher, whereas long term rates, which had been rising started falling (we’ve also seen a comparable effect in commodity markets with oil for immediate delivery generally increasing in price, but oil for future delivery not keeping pace).

Short terms rates should strictly mean 90 days or less for US Treasury Bills but in practice are described for up to say 3 years in duration while long term bonds are those of 20 years or more.

The price of a bond falls when interest rates or yields on bonds go higher and the price of a bond rises when yields go lower.

This creates the slightly counterintuitive situation that bond investors (bondholders) benefit if interest rates fall as the price of their bonds rises (the same concept also generally applies to the value of investment property).

All of this is telling us that not only is the recent supply shock (akin to a speed skid mark in the post-Covid opening) every bit as transitory as policymakers such as the Fed continue to insist, but it also implies, especially in the case of treasuries, that policymakers might make the future situation even worse than it would otherwise have been.

‘The divergence didn’t begin last month- we can see that it took root back in late January’

If short term policy rates rise (because the Fed Open Market Committee [or “FOMC”] is worried about inflation), that can dissipate short term inflation worries but it will also put a brake on longer term economic growth.

In other words, increasing short term rates right now leads to lower long -term rates because of the perceived feedback loop in the future from higher interest rates today acting as a drag on future growth, especially if it reaches the stage that long term rates fall below short-term ones (an inverted yield curve, which typically indicates a coming recession), although we’re not at that stage yet.

Morton’s Fork’ implies that opposite actions might result in the same outcome

Cardinal John Morton was a leading lawyer, who played a significant role in establishing the Lancastrian claim following the Wars of The Roses and was rewarded by being appointed Archbishop of Canterbury and also Lord Chancellor of England under Henry VII. As if lawyer, Lancastrian, prelate, and politician isn’t a big enough charge sheet against him, Henry tasked Morton with raising and collecting taxes to restore the royal coffers.

Morton's tax policy, carried out by his loyal lieutenants Dudley & Empson, became known as Morton’s Fork - if his agents were welcomed lavishly by an estate, they levied high tax bills on the basis that the estate could clearly afford it whereas if they encountered austerity, they levied equally high taxes on the basis that, by different logic, the estate could clearly afford it.

"If the subject is seen to live frugally, tell him because he is clearly a money saver of great ability, he can afford to give generously to the King. If, however, the subject lives a life of great extravagance, tell him he, too, can afford to give largely, the proof of his opulence being evident in his expenditure."

Morton may also have played a significant role in the demonisation of Richard III that largely grew from the accounts in the popular work of propaganda written by his protégé, Thomas More, that discredited the former Yorkist leader with dubious claims that he had murdered the ‘Princes in The Tower’.

Where the fork comes in is that we seem to have reached the point where not only would higher short-term interest rate expectations continue to cause long term rates to fall but also if short term rates fall again, because of concerns over weaker recovery, then this time this could have the effect of dragging down interest rates of all durations. In the current situation, we think that this would have the greatest impact on long term bond rates.

When this happens, rather like Cardinal Morton’s Fork, it implies that opposite scenarios might result in the same outcome.

The biggest difference is perhaps that while in the fifteenth century Morton used his ‘fork’ to transfer wealth to the treasury. At least any reduction in today’s long term interest rates will increase the price of long-term government bonds, generating returns for investors who are holding long term government securities. We had already preferred longer-term over short-term treasuries and recommend a portion of these as a key cornerstone risk hedge in a portfolio.

Footnote

Some commentators (by which I really mean me - and to some extent the team but mainly me) have been extremely critical of some members of the Fed, referring to the Fed’s ‘Hawkish Caucus’ as its ‘lunatic fringe’ and firing in their direction Prof. Steve Keen’s criticism of neoclassical economists as being ‘Ptolemaic astronomers in the age of Copernicus’.

However, debit where debit is due.

In the minutes released this Wednesday, the Fed learned from last month’s debacle.

Instead of giving insights into the misguided things that the Fed committee members said, the current minutes tended to say instead that such and such an issue ‘was discussed’.

The critical thinking may not be getting better but the minute taking is getting more market friendly.

Except on the one thorny note of whether, in view of the frothy/bubbly/overheated US housing market, the FOMC should taper the buying of mortgage securities (which date back to a programme introduced in 2009 to support the then struggling US housing market) more aggressively than they should taper buying of treasury securities. They actually shouldn’t taper until they can inject funds directly into the economy (People’s Bank of China style). But if they do taper, pretty much everyone agrees that mortgage securities should bear the brunt. But this week’s minutes suggest that this is unlikely - mainly for the particularly good reason that The FOMC hadn’t thought of this before so, they don’t really want to have to start thinking of it now.

After all, in a Ptolemaic system, everything does revolve around them….

How should you position your portfolio?

MBMG Investment Advisory is licensed by the Securities and Exchange Commission of Thailand as an Investment Advisor under licence number Dor 06-0055-21.

For more information and to speak with our advisor, please contact us at info@mbmg-investment.com or call on +66 2 665 2534.

About the Author:

Paul Gambles is licensed by the SEC as both a Securities Fundamental Investment Analyst and an Investment Planner.

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit, it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledge all risks and have been informed that the return may be more or less than the initial sum.

Copyright © 2021 MBMG Group, All rights reserved.

Our mailing address is:

MBMG Group | 75/56 Ocean Tower2, 26th Fl., Soi Sukhumvit 19(Wattana),

Klongtoey Nua, Wattana, Bangkok 10110 Thailand