MBMG Investment Advisory Report and Outlook January 2022

Past the peak?

One issue has been bothering us for the last month – inflation.

Actually, it’s been bothering us for longer than that but for different reasons.

The consensus view is that the world has an inflation problem.

We agree.

The consensus view is that inflation is too high.

We’re not so sure.

The consensus view is that policymakers need to hike interest rates and reduce the injection of government funding into both the economy and capital markets.

We definitely disagree.

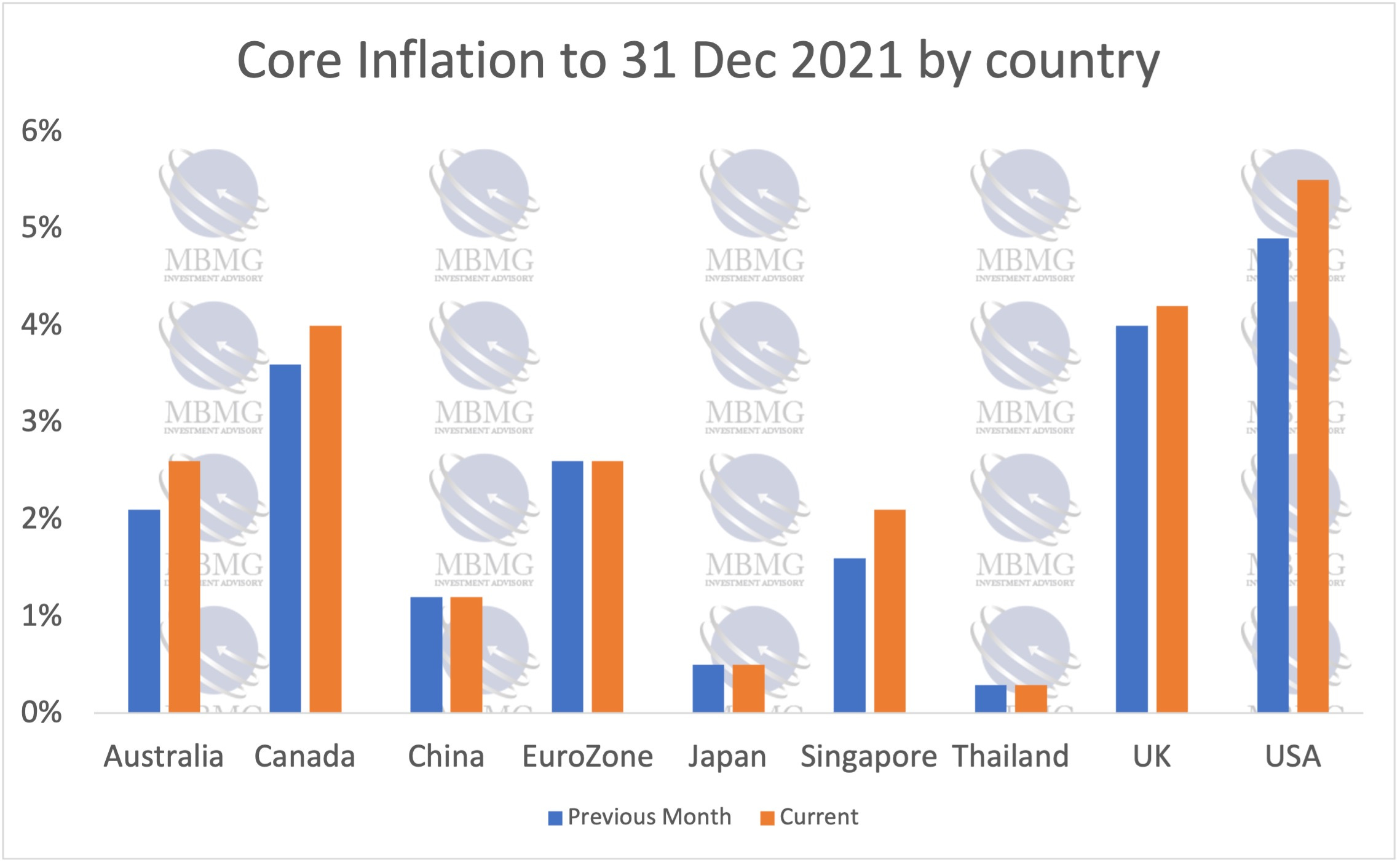

Before you read this section and look at the chart on the following page, ask yourself what you think the annual rate of inflation is in Thailand, Europe, USA and whether this has changed recently.

Definitions of inflation are problematic – no two individuals or households spend in identical patterns, therefore, not everyone is affected in the same way by changes in price of goods and services. This varies hugely within countries (patterns of spend being dictated by personal preferences, availability of disposal income and lifestyle considerations – a family that has high disposable income has different priorities and different capacity for expenditure, than a single individual with no source of income) and also from country to country.

The least unreliable way to capture meaningful inflation trends could be argued to be core inflation, which typically excludes the cost of food and energy.

This is in many ways a nonsensical measure because I don’t know anyone who doesn’t have to spend money on food or energy, but absent any better choices it may be the least bad measure-

How does this compare to what you’d expected?

We suspect that it’s lower in many cases than people perceive from their own experience.

The outliers (major economies where inflation is above 3%) are Canada, USA, and UK - we could have also shown Russia (8.09%), Brazil (7.3%), Mexico (5.5%), Germany (3.7%) & South Africa (3.4%), which along with perennial inflation basket cases Argentina (55.5%) and Turkey (31.9%) are the only G20 nations above 3% (Netherlands, Spain, France, Indonesia, Italy & Switzerland are all under 2.5%).

Turkey and Argentina are specifically currency related.

The structure of Brazilian trade has long left the country particularly susceptible to supply chain shocks and Russia’s woes are largely driven by a combination of sanctions and a weaker Ruble.

German inflation reflects a number of technical factors – most notably base effects being exacerbated by the reintroduction of the normal rate of VAT, which was reduced a year ago as a policy to help reduce consumer costs during the lockdowns.

South Africa has suffered extreme supply chain disruptions during COVID, especially during the most recent variant.

The UK appears to have suffered from significant post-Brexit supply chain issues as well as a perceptible recent fall in the Pound.

These might be considered idiosyncratic issues but this leaves, Canada, the USA & Mexico, or what we might call USMCA ( United States–Mexico–Canada Agreement, the successor to NAFTA ushered in by Donald Trump) inflation.

Why are these countries suffering such high inflation?

Although there are many complicated components to any inflation reading (part of what makes them so unreliable), it seems that a number of factors have made USMCA inflation, especially US inflation so severe-

The US is by far the biggest consumption economy – although ‘only’ comprising around 5% of global population, America consumes one-third of the world’s and 27% of metals like aluminium (even if Americans can’t pronounce it properly to English ears), as well as other materials, minerals, and resources. America is also largely dependent on imports – so while other countries, such as China are major consumers of timber, none are as reliant on imports.

This has made USA particularly vulnerable to supply shock.

Housing costs have increased significantly for a variety of reasons, but largely due a lack of inventory to meet the post-pandemic demand that may have been partly driven by such low interest rates, but also due to construction constraints because of supply chain issues.

American economic policy during the pandemic has been to support consumption by issuing ‘stimmies payments’ directly to individuals and families. This has disguised some of the demand challenges and also had the reported effect of giving US employees slightly more bargaining power about when to return to the workplace (this may still be very heavily loaded against employees, but inflation merely charts the direction, not the absolute level of employee bargaining power in wage effects).

So, the biggest idiosyncratic factors in the only major instance of global inflation are that a consumer society has managed to keep consuming during a global shutdown but, being a primarily importing economy, has been out of synch with disruptions to global supply. From timber price volatility to microchip shortages to shipping capacity, this theme has been exceptionally well-covered, especially from a US perspective, by the Odd Lots Podcast in the last year or so https://www.bloomberg.com/oddlots-podcast?sref=3ULs2uPI

Sadly, we suspect that US policymakers have not been listening.

A late, but strong contender for the most ill-informed tweet of 2021 was this from Mitch McConnell-

While there are so many things that are wrong about it, the key point is that the inflation that we’re seeing isn’t a reflection of excessive spending but of disruptions to supply. US consumption in 2021 is likely to have been at similar levels to 2019. Admittedly, this is a healthy recovery from the dip of 2020, but still reflects no net increase in spending for 2 years (the rest of the world in comparison managed to increase during that period, nowhere more so than China, where, despite achieving growth close to double digit across the two-year period, inflation remains muted at just over 1% per year.

Not only has the US economy stagnated but policymakers now seem to be putting it in a neck-hold and cutting off its oxygen supply, by reducing asset purchases and threatening to hike interest rates. The real danger is that this will widen the fork between the rapidly slowing former dominant economies, such as USA & UK and the steadily growing developing economies of Asia, where we expect policymakers to adopt a much more pragmatic approach. This could be a pivotal moment in economic history.

Request OUTLOOK Report 31st January 2022 : Past the peak?

Recent Updates From MBMG

Sign up for MBMG newsletter from MBMG

MBMG Investment Advisory is licensed by the Securities and Exchange Commission of Thailand as an Investment Advisor under licence number Dor 06-0055-21.

For more information and to speak with our advisor, please contact us at info@mbmg-investment.com or call on +66 2 665 2534.

About the Author:

Paul Gambles is licensed by the SEC as both a Securities Fundamental Investment Analyst and an Investment Planner.

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit, it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledge all risks and have been informed that the return may be more or less than the initial sum.