MBMG Outlook - Rock and Roll Winter?

31st December 2021

Executive Summary

2021 was another year, arguably the 3rd in succession, where risk-taking was once again rewarded. The highest risk assets generated strongly positive returns, zero risk assets generated nothing (or at most a rounding error) and low risk assets lost money during the course of the year.

The long-term runes continue to indicate weak economic activity, transitory inflation, and anaemic interest rates. In ‘Technicalities,’ we explain the significance of money creation in a post-QE world, why the Fed’s and Treasury’s stated policy course of tightening both fiscal and monetary policy would be disastrous (eventually) for risk assets. Finally, we also show that fortunately their words are currently at variance from their actions.

This leads us to conclude that “2022 looks as though it could be a ‘game of two halves' in which “the first half could benefit from the continuation of positive momentum, whereas the second half could see that derailed by the withdrawal of liquidity from capital markets. However, both of these assumptions are very much subject to changing conditions and 2022 is the year when strategy will need to evolve and adapt alongside those changes.”

We don’t know when Covid will pass but we do believe that at some point, possibly very soon, possibly not, it will. However, the problem of extreme debt, inequitably distributed, is persistent and, within the current policy framework, unremitting. This creates contradictory forces but at a time when the prices of risk assets allow very little margin of error.

2022 is a year when we recommend paying constant attention to economic indicators and asset prices and adopting an active, adaptive, and pragmatic approach to asset allocation, even more so than in the year just passed, when such an approach proved essential to achieving acceptable returns without taking on extreme risk.

Asset Class Observations

The year proved challenging for defensive assets and therefore for genuinely cautious or low risk portfolios. In many ways, the last 3 years have seen risk taking rewarded.

The most risk free of all investable asset classes (90-day treasury ETFs) returned 0.01% for the year, with little, if any, premium paid on good quality deposit accounts. Duration was penalised with intermediate treasuries losing 2.4% whereas long term treasuries lost 5.9% for the year. Even in fixed interest, risk was again rewarded as investment grade corporate bonds (LQD) lost 1.8% for the year whereas high yield and junk returned profits (HYG 3.75%, JNK 3.99%).

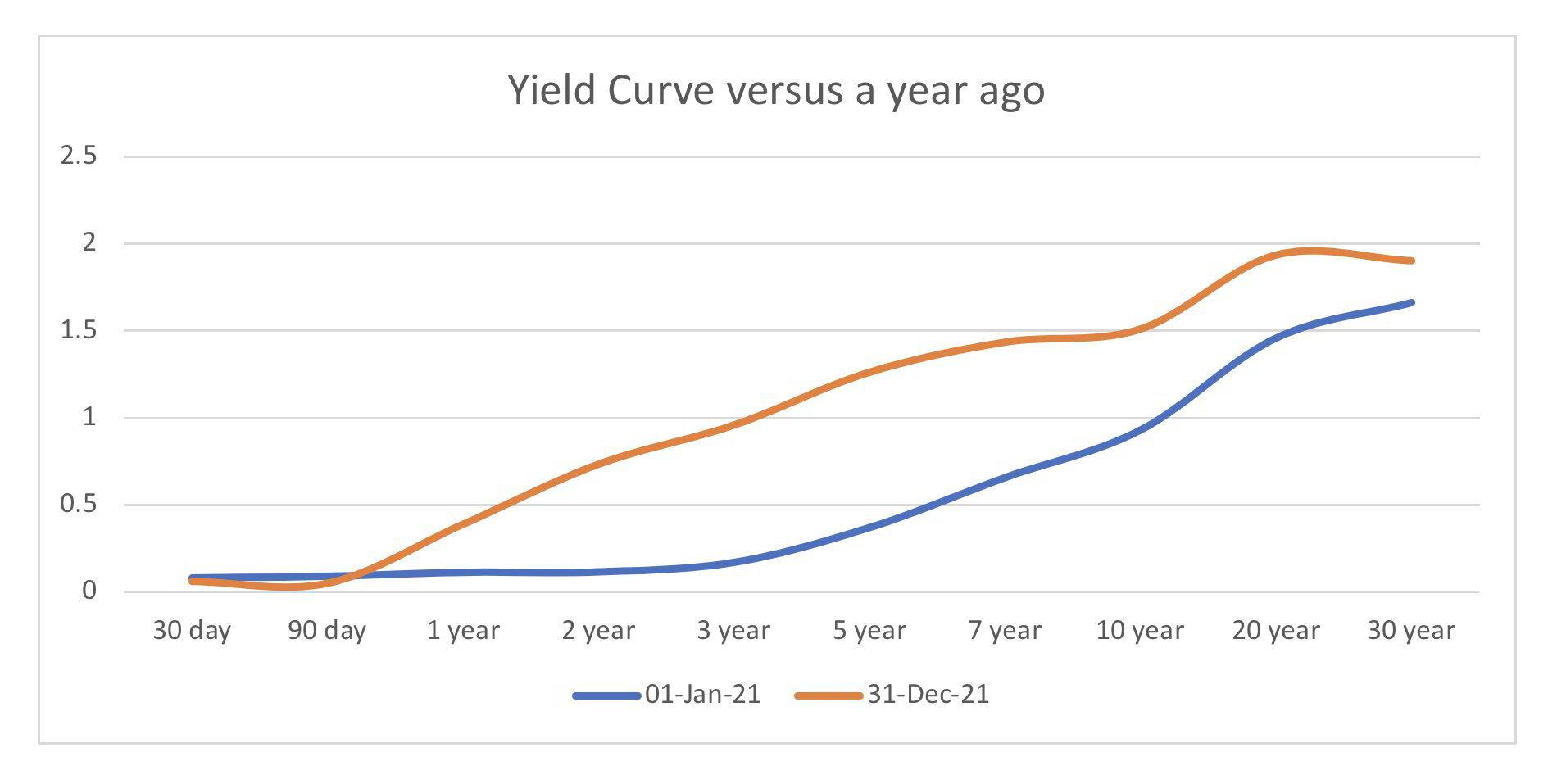

The yield curve flattened appreciably as the year has progressed. The anchoring of long-term treasuries, where the move up has been greater than any other major treasury bond duration.

When we also consider the implied break-even inflation, which in the post-COVID rebound has failed to break above 2.4%, which, if it continues to do so, implies that structural disinflation, along with constrained inflation and growth expectations remains in place, as it has since 2013:

This indicates that inflation fears may be overdone, growth expectations may be too great and would validate the view that we have held throughout 2021; namely that policy interest rate increases are not justified by economic conditions. If this view continues to be supported by bond market expectations and ultimately to be validated, then long-term treasuries should offer reasonable returns and strong diversification to growth assets from here (iShares 20+ Year Treasury Bond ETF would need to increase in price by over 15% from here to regain its peak of last year, whereas PIMCO 25+ Year Zero Coupon U.S. Treasury Index Exchange-Traded Fund would need to increase by over 22.5%).

We recommend a highly adaptive allocation to these assets – if bond markets’ expectations are wrong and long-term growth and inflation expectations are insufficiently robust, then rates will move sustainably higher, and our thesis will have to be abandoned. Conversely, if our thesis is ultimately validated, it seems unlikely, in view of the prevailing volatility, that this would happen in a straight line from here. The PIMCO ETF has fallen by over 7% from its peak of 4 weeks ago – this is extreme volatility in terms of treasury pricing. This creates opportunities that can be exploited by buying into relative dips and decreasing at higher levels. At some point, long treasuries might break out and lightening up might leave some opportunity on the table but for this year, such active position management has enabled our clients to generate profits from an asset that has actually fallen in value by over 5% compared to a year ago.

Similarly, gold has endured a difficult year with gold falling by 15% in the first quarter of the year and gold miners down by over 20% in the first 2 months. Since then, both have rallied back into positive territory before falling again (the gold mining ETF, GDX, showing a year-to-date loss of over 25% just prior to the end of quarter 3, with gold re-testing the March lows). The subsequent rally has been volatile and unconvincing (GDX had barely recovered just a couple of weeks ago before ending the year 16.8% lower than it started, while gold is down by 6.2%. Again, assuming that market expectations of low growth, disinflation and low interest rates are validated, then this is a positive backdrop for gold and gold miners. In addition, they also provide strong diversification benefits to growth assets. Analogously long-term treasuries, if expectations are wrong and interest rates move sustainably higher, our thesis will have to be abandoned, whereas if our thesis ultimately validated, it is unlikely to happen in a straight line from here and therefore the adaptive approach to dip-buying and profit-taking on gold and gold miners could continue at least through the first half of 2022.

Currencies have generally behaved as we expected – although USD strength substantially materialized only from mid-June onwards. Again, if the market expectations and our contingent thesis about weak growth and weak inflation is ultimately validated, then we’d expect USD to significantly strengthen from here, especially against Euro and also deficit currencies such as AUD. However, if not, then we should expect to see EM currencies in particular outperform and also possibly AUD if H1 22 data such as deficits are better than estimated. Even in the event of ultimately continuing USD strength, the recent surge in USD has set up the high risk of a counter trend pullback during the first half of 2022. Short term FX exposure may be too difficult to call – any weakness in USD, without indicia of higher growth emerging, could be a buying opportunity.

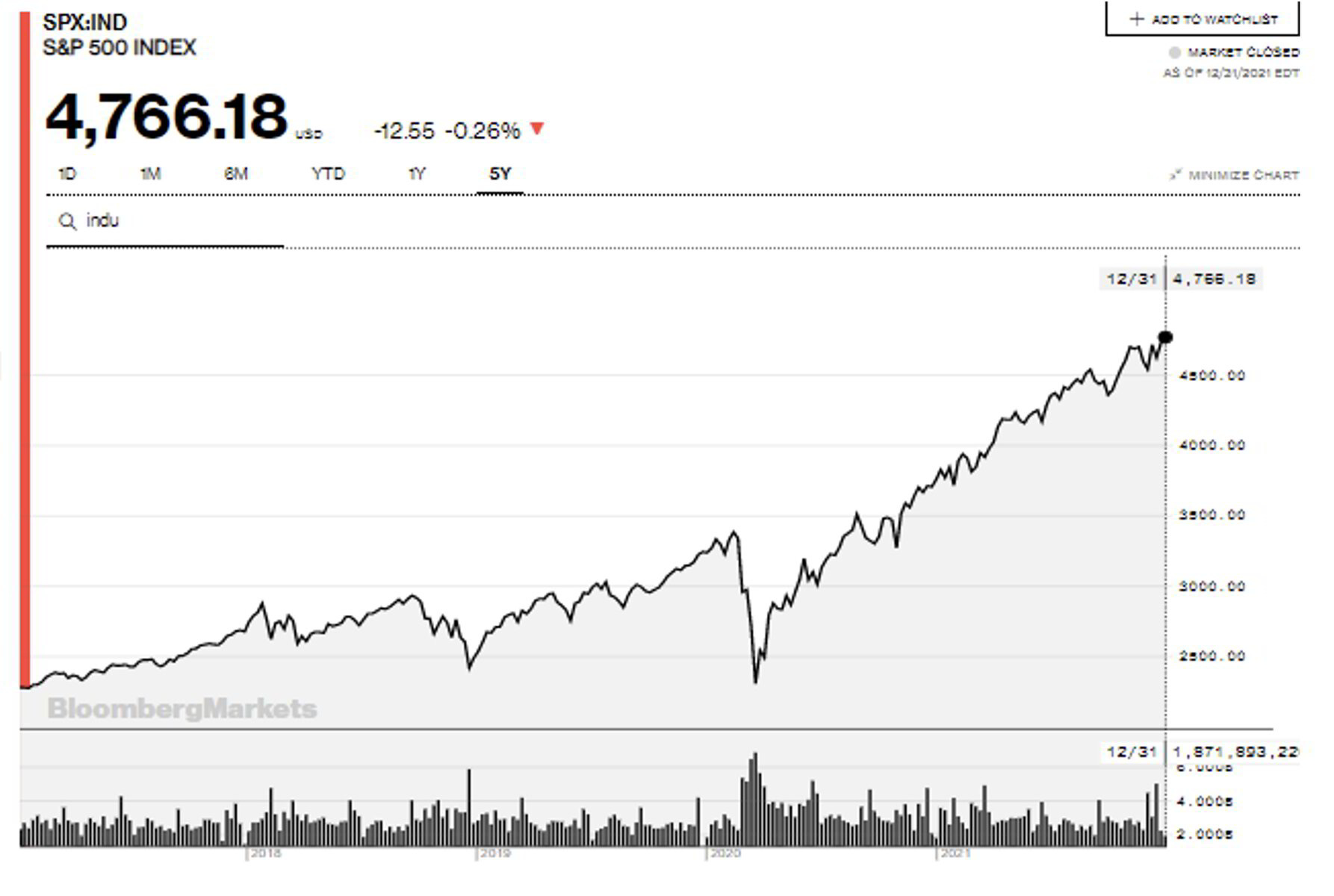

Risk assets – such as equities, corporate bonds, and property, look extremely richly valued. The S&P 500 has more than doubled from the low point in March last year and has done so in a straight line (see chart below). While the NASDAQ Composite has strongly outperformed the broader index during this period, it’s notable that since Valentine’s Day, the broader index has reclaimed leadership, increasing roughly double the 10% that NASDAQ has increased, with the industrial stocks that dominate the Dow Jones, falling in between.

If bond market expectations come to pass, then these extreme valuations look ultimately unsustainable. While our base case (but with very low conviction) is that good news on COVID will support earnings momentum into the first half of 2022, unless we see a shift in long term expectations, then at some point earnings will fail to grow sufficiently to support risk asset valuations. This is particularly worrying in the current policy environment, which should see liquidity gradually dry up.

However, as we discuss in this report, liquidity conditions remained extremely supportive into the year end. If we listened to what the Fed & Treasury were saying, we’d be worried about a major risk asset correction in the coming months. If we look at what they’re actually doing, it seems as though they haven’t yet started that particular alarm clock, or maybe time bomb, actually ticking.

We can only watch for when they do and hope that earnings sustain until then and that the rally built on foundations of sand continues. But hope is not a strategy and therefore, we’re happy to continue to sacrifice potential return in the name of risk management by resorting to significant degrees of hedging in our portfolio advice.

For some time, it has looked as though something must give. Policymakers are saying that they have blinked because of inflation but so far this is more head fake than reality. If it does become reality and if we don’t see any improvement in structural economic weakness, then the risk-taking that has been encouraged and rewarded could be very seriously punished in months or, more likely, years to come.

DOWNLOAD MBMG OUTLOOK

31st December 2021 Rock and Roll Winter?