More or less.... (Part Two)

In Part One (https://mbmg.substack.com/p/more-or-less-intelligent) we explored the possibilit that exposure to increasing amounts of data may increase rather than reduce the risk of narrative fallacy.

In this conclusion, we examine how this is currently affecting capital markets - how it is creating additional risk in developed market risk assets and opportunities elsewhere (such as recently downgraded US Treasuries, the dip in JGBs and the Yen and also in underperforming Chinese domestically focused equities).

The narrative fallacy is the tendency to create a story with cause-and-effect explanations out of random details and events. We fall victim to the narrative fallacy because our brains want to make sense of a random world – Thinking, fast and Slow – Daniel Kahneman

We see examples of narrative fallacy pervading capital market thinking right now. The idea that developed market equity prices are rising because the economy is performing well (and specifically that western policy has engineered a soft-landing) is a prime example of Occam’s Razor. There are many factors that can cause stock prices rise. The prevailing narrative appears to be that the current market buoyancy is due to a combination of falling inflation and robust economic, especially employment data. We’d question these assumptions.

Are you saying that the stock market bounce has other drivers?

We believe that this narrative is ignoring other drivers of the recent rally. In particular, the forced induction of the best part of a trillion Dollars into the US financial system by policymakers in a crazy week or so in March when the US regional banking system seemed to be at risk of collapsing due to policymakers’ earlier efforts. Capital uses neither inductive nor deductive logic – it simply flows to the places that will offer returns. On March 13th the S&P 500 index fell into negative territory for the year to date, reaching a low of 3808. Within a couple of days, the Fed balance sheet reflected the firefighting efforts of policymakers (at the Fed, they fight fires in capital markets by throwing Dollars on them)

We can see the scale of this by looking at the weekly assets of the Federal Reserve System, which have been declining since the Fed Open Market Committee (FOMC) decided to reduce the size of the Fed balance sheet by selling assets. The chart on the following page shows this from the beginning of February to the end of March-

If we zoom out, we can see that this was the 3rd precipitous action of this kind (the previous two were used to support markets and the financial system during the Global Financial Crisis [GFC] of 2008-9 and during the Great Lockdown of 2020.

Each previous action sparked a major equity market rally but also created such a dependency on this source of market capital that policymakers attempts to reverse the policy were unsuccessful and resulted in unwanted effects that forced policymakers to ‘turn the taps back on again.

Of course, during the great bull runs that coincided with the taps being fully open, many other explanations for market exuberance were touted, although it’s far from clear to us that any of these have exerted anything like the same degree of influence as the Fed backstopping markets in this way.

However, that raises a number of uncomfortable questions about the purpose of policymakers – are they answerable to the people at large or to capital market interests?

We all know that the answer is the latter but as Henry Ford famously said, “It is well enough that the people of the nation do not understand the banking and financial system, for if they did, I believe there would be a revolution before tomorrow morning.”

In other words, we have alignment of systemically conflicted interests to ensure that the idea that policymakers are doing a great job for everyone, to further obscure critical analysis of their policies.in addition to the challenges of disaggregating and interpreting huge volumes of data, we also have conflicted interests happy to disseminate a narrative designed to ensure that there are no revolutions before tomorrow morning.

Changes in economic and capital market activity have been proven to be primarily responsive to relative net inflows – which makes sense – if more money chases assets, those assets inevitably increase in price. In the interests of thoroughness, we do therefore also have to consider the other source of money in the economy and capital markets, namely commercial banks. The chart below aggregates commercial bank assets and Fed assets, over the last two years, but we can see that the effect is the same (aggregate USD value is the grey line, left hand axis, % change is the orange line, right hand axis):

The financing activities of the Fed during March stick out like a sore thumb.

However, it’s also apparent that the grey line, the aggregated assets of commercial banks and the Fed are now back to the levels that they were when March’s mini crisis erupted. Maybe the regional banks are now better able to withstand the liquidity drain that was such a challenge just five months ago. However, it seems very dangerous thinking to exclude from market outlook the primary factor that has driven the S&P500 almost 17% higher and the NASDAQ 24% higher, especially as that driver is now being taken away.

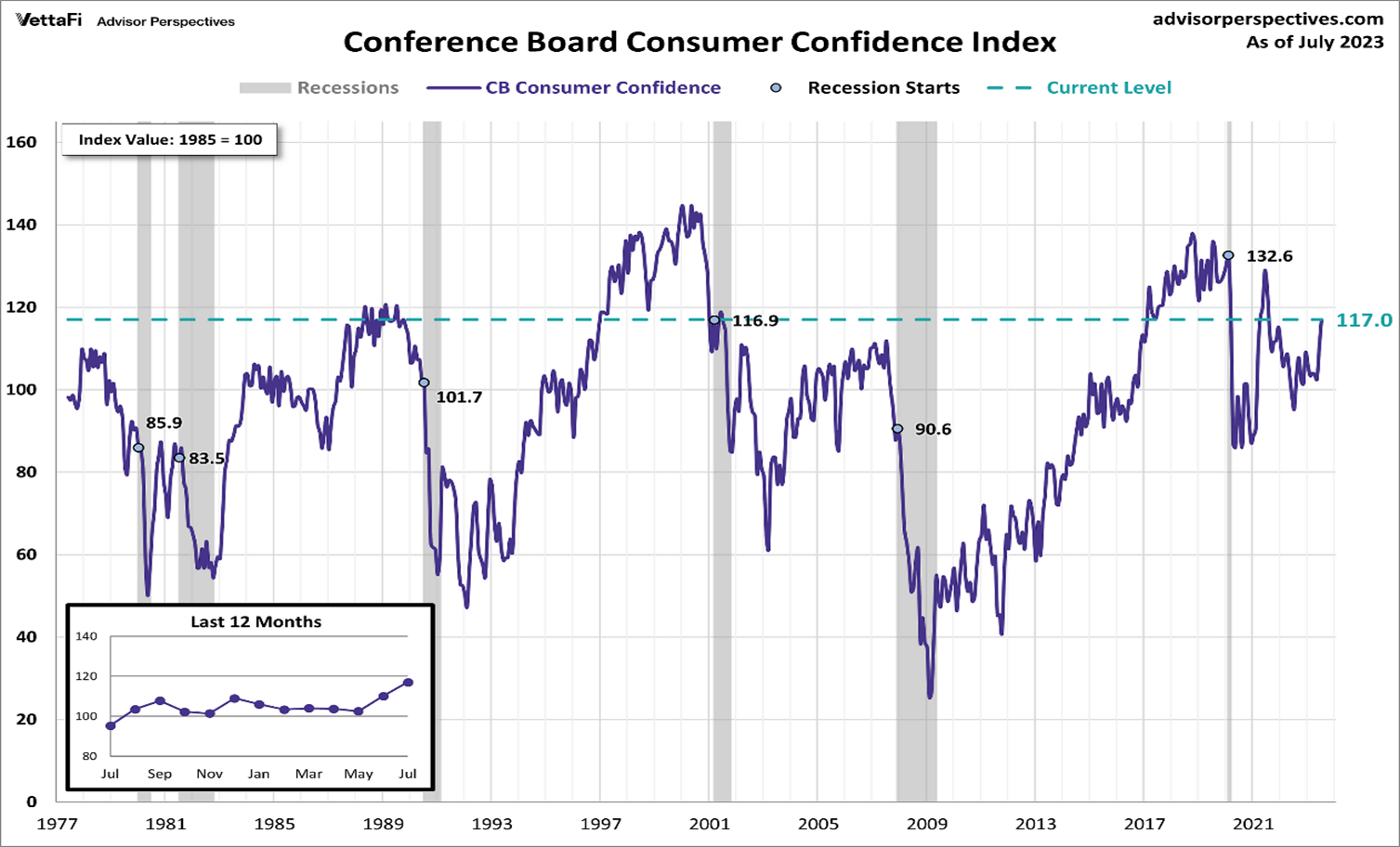

But what about all the other positives? Look at consumer confidence?

It also seems flawed to us to rely on factors that are essentially a derivative of this driver. Trumpeting that consumer confidence is at a two year high, largely ignores that this is a consequence of the rally in capital markets and the recent sharp leg up pretty much dates back to that, allowing for the expected lag between equity market bounces and consumer sentiment:

Then what about the employment story? Surely, that isn’t just a derivative of the Fed’s Spring mini-bailout?

Maybe not (although there is a stronger historic correlation between employment and money creation - also known as credit impulse- than just about any other factor).

However, the key point is that employment is another widely misunderstood indicator of economic health.

The blue line in the chart on the following page represents the official jobless rate in America during the last 75 years.

The grey bars indicate recessions. As can be seen, the cyclical low points in unemployment have typically presaged recessions.

Low unemployment is unquestionably desirable. It is however, also one of the most reliable indicators of impending recession, especially when it appears to have bottomed out. This holds true from the 1950s through to the GFC and the Great Lockdown:

In other words, the strong US labour market should be touted more as a leading indicator or impending recession than a signal of economic strength.

Ok, so what about the fact that inflation is falling? Surely that’s good news for the economy and for markets and for businesses?

Potentially yes – in that it would allow policymakers to take a victory lap claiming that they had overcome inflation and this could presage much more accommodating monetary and fiscal policy. There’s no doubt that inflation is receding by just about every measure that can be used:

The reduction in inflation by itself should not however be seen as an unadulterated positive for capital markets. Falling inflation is likely to mean falling corporate margins, which impacts corporate spending, hiring and investment as well as worker salaries. There is no clear and obvious indicator that falling inflation by itself feeds through to economic activity or corporate earnings in a directly beneficial way (the redline below is the rate of inflation, the grey areas are, once again, recessions):

That said, a return to Fed ‘sponsorship’ of capital markets of the kind that dominated the western policymaker landscape (it’s not just the Fed, other developed nations undertook similar policies although to less egregious extents) after the GFC, that might be expected to enable the continuation of the capital market rebound that appears to have started in March, pump-primed by Fed liquidity. The two situations that would enable a resumption of that would be either the sufficient reduction in the rate of inflation for policymakers to be able to declare victory over inflation or a crisis of the kind that forced the Fed to act earlier this year.

The tough rhetoric of policymakers combined with the various measures of inflation remaining sufficiently elevated above policymaker target levels suggest to us that it may well be that the need to react to a crisis will precede the inflation beating victory laps. This means that there is a very high risk of asset price corrections from here.

So, things look really bleak?

Actually, we’re not saying that. Not in those terms. We’re aware of prevailing narrative fallacies that claim that there is a great opportunity in risk assets and we’ve tried to understand why these fallacies are so widely believed.

So what we are saying is:

· Many of the explanations as to why risk assets have rallied strongly and will continue to rally lack a solid, deductive basis.

· Worse than that, many of the justifications indicate that risk assets could fall sharply in price.

· These fallacies are priced into current valuations which makes risk assets objectively expensive, vulnerable to re-pricing.

· Further price appreciation is certainly possible BUT this would require either an extension of the mispricing (even greater fallacy) and/or a genuine price justification whiIn fundamentals this month, we explored the way that exposure to increasing amounts of data may increase rather than reduce the risk of narrative fallacy.

· This mispricing primarily applies to developed market risk assets – we don’t see the same fallacies or the same mispricing in assets such as long-term US treasuries or in Chinese and other emerging market risk assets which do not appear to have significantly benefitted from the factors that have driven western risk assets higher.

Recognising narrative fallacies built on faulty human intelligence doesn’t confer an ability to foretell the future. It does however help to prevent misjudgements in the present.ch we’re currently unaware of and which doesn’t feature prominently in market analysis that we have seen.

MBMG Investment Advisory is licensed by the Securities and Exchange Commission of Thailand as an Investment Advisor under licence number Dor 06-0055-21.

For more information and to speak with our advisors, please contact us at info@mbmg-investment.com or call on +66 2 665 2534.

About the Author:

Paul Gambles is licensed by the SEC as both a Securities Fundamental Investment Analyst and an Investment planner.

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit, it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledge all risks and have been informed that the return may be more or less than the initial sum.