Spaced Out

The 5th and thankfully final part of why we see the IPO SpaceX as a launch pad to disaster

Spaced Out

Elon Musk and Ivar Kreuger - a match made in….?

Space is the ultimate Unicorn: it represents an infinite, boundaryless total addressable market (TAM) of pure, unadulterated upside, yet its actual revenue model remains a mystery. Like a classic SoftBank venture, the strategy is to out-inflate the valuation, secure a legendary founder, and let the narrative (and the financial engineering) do the heavy lifting.

The Strategy: “Space” as a Vision-First Unicorn

Venture capital thrives on the premise of paying exorbitant multiples for “future execution”. Space checks every box on the late-stage funding bingo card.

The TAM is Literally Infinite:

You aren’t just an “office landlord” or a “software provider”—you are an Everywhere-Universal-Master-of-Space. When the market demands gargantuan scale, there is no bigger sandbox than the cosmos.

The Narrative Founder:

We need an idiosyncratic, visionary founder who speaks in grand, quasi-spiritual missions about saving humanity or elevating consciousness. Whether the business model currently prints cash is irrelevant. As Bloomberg columnist Matt Levine has famously detailed with “Unicorns,” the goal is to make the story so compelling that traditional metrics (like EBITDA) feel quaint and outdated.

Ramping Valuations: The Masayoshi Son Playbook

When nobody knows exactly what the product is or how it will turn a profit, the SoftBank technique is perfectly deployed.

The Series A Ramping

You raise a seed round on the premise of “The Cosmos.” Six months later, you raise a Series A at a $10 billion valuation simply because a charismatic founder pitched a slightly shinier rocket.

Illiquidity Preference & Markups:

You don’t exit to the public markets via a traditional IPO; you rely on massive private capital injections to keep the music playing. Every time you sell a sliver of the company to a sovereign wealth fund or a massive Vision Fund, the paper valuation doubles.

Circular Narrative Reinforcement: The value becomes whatever the last investor paid, plus a healthy hype premium. The goal is to meme the company into legitimacy, allowing early investors and visionary executives to diversify before the wider public realises that deep space is mostly a vacuum.

The value is whatever the last guy paid for it, plus a healthy 40% hype premium. The ultimate goal is to “meme” the company into legitimacy, allowing the original investors and visionary executives to diversify their holdings before the broader public realizes that deep space is mostly a vacuum.

The Annoying Details

A masterclass in modern financial architecture: selling a tiny fraction of a company to create a massive paper value for the rest. By selling a $75 billion float, which represents a mere 4.3% of the company’s total equity, SpaceX locked in a public share price of $135. When you multiply that single $135 data point across the remaining 95.7% of tightly held, untraded internal shares, you instantly conjure a $1.77 trillion market capitalization. In other words, $75 billion invested into SpaceX IPO somehow made the existing shareholders $1.77 trillion wealthier. This speaks to Ray Dalio’s point that they might claim to feel $1.77 trillion wealthier but, unless someone lends against the value of the remaining $1.7 trillion paper value, then it’s not real. Except that banks will lend against that. So actually what happened with the SpaceX IPO is that the supposedly richest man on the planet just got the license to borrow more money. Which might be useful. After all, he still owes the banks $13 trillion that he borrowed to buy Twitter. Which was partly secured on his Tesla holdings. Which would be a worry if it were linked to Tesla profitability:

2022 | ████████████ (12.6)

2023 | ███████████████ (15.0)

2024 | ███████ (7.2)

2025 | ████ (3.8)

2026 | ████ (3.9)

But somehow Tesla’s stock price, is now 250% higher than it was at the 2023 low, which means that it’s only 1% lower than it was in November 2021 (no, it doesn’t pay a dividend – apparently, it’s a growth stock).

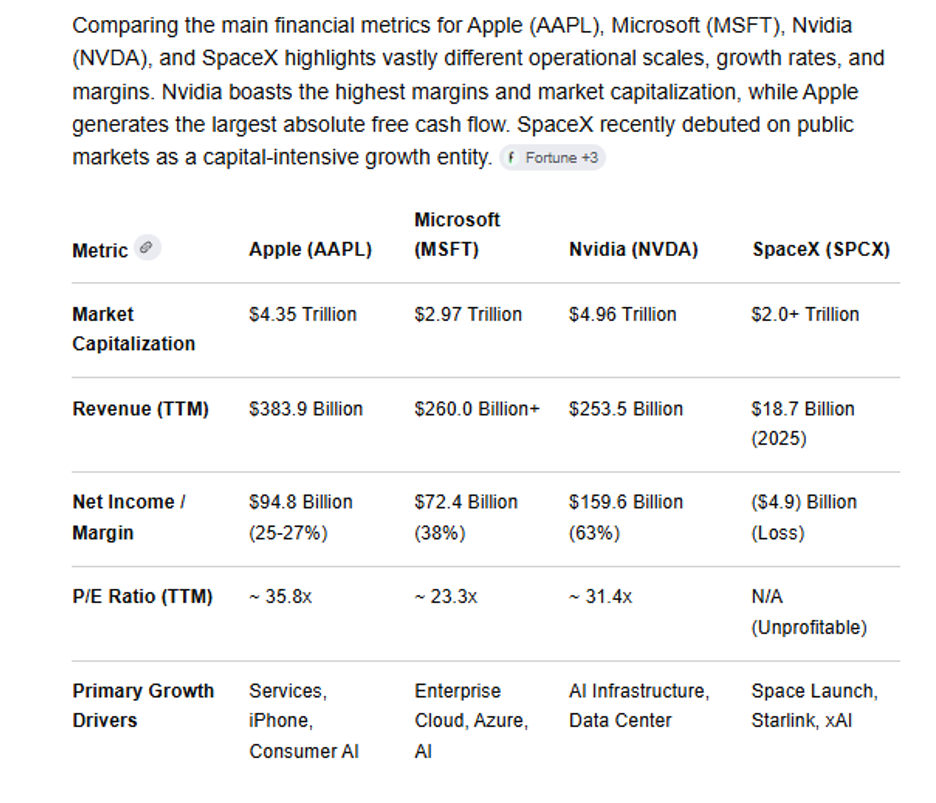

But that is all dwarfed by what Elon can now borrow against the company that somehow listed for $1.77 trillion and whose pretend market capitalisation value, on its second day of trading now approaches $ 2.5 trillion. In other words SpaceX is now, by the pretend market cap metric, the 4th largest company in the world. However, using any other metric it doesn’t really stack up, as the following (AI-generated) table highlights:

Gemini’s summary of SpaceX’ valuation is succinct:

SpaceX (SPCX): SpaceX trades at a high premium equivalent to legacy mega-caps but is currently a cash-burning entity. Investors are pricing in anticipated growth in space-based connectivity (Starlink) and enterprise artificial intelligence over the next decade.

You might wonder why Elon ‘only’ listed 4.3% of SpaceX. That single listingis in and of itself the largest IPO ever, massively outpacing the $29.4 billion raised for selling 1.5% of Saudi oil giant Aramco in 2019. Interestingly the next 2 biggest raises were Ali Baba on the NYSE in 2014 and Ali’s main sponsor and our old friend, Softbank on the TSE in 2018. The Softbank playbook has clearly been dusted off one more time – list what you can at the highest possible price and then use the rest as security with gullible banks. In that respect, Elon Musk has never looked more like Ivar Kreuger.

The Illiquidity Illusion

The narrative that Elon Musk is now “the world’s first trillionaire” or that the IPO instantly minted thousands of liquid millionaires ignores the fundamental mechanics of market liquidity.

Extrapolation vs. Actual Liquidity

A valuation is not a bank account. A $1.77 trillion market cap means that a tiny, highly enthusiastic pool of buyers was willing to pay $135 for a small sliver of the company. It does not mean there is $1.77 trillion of cash waiting to buy out Elon Musk or his early investors.

What does SpaceX actually do?

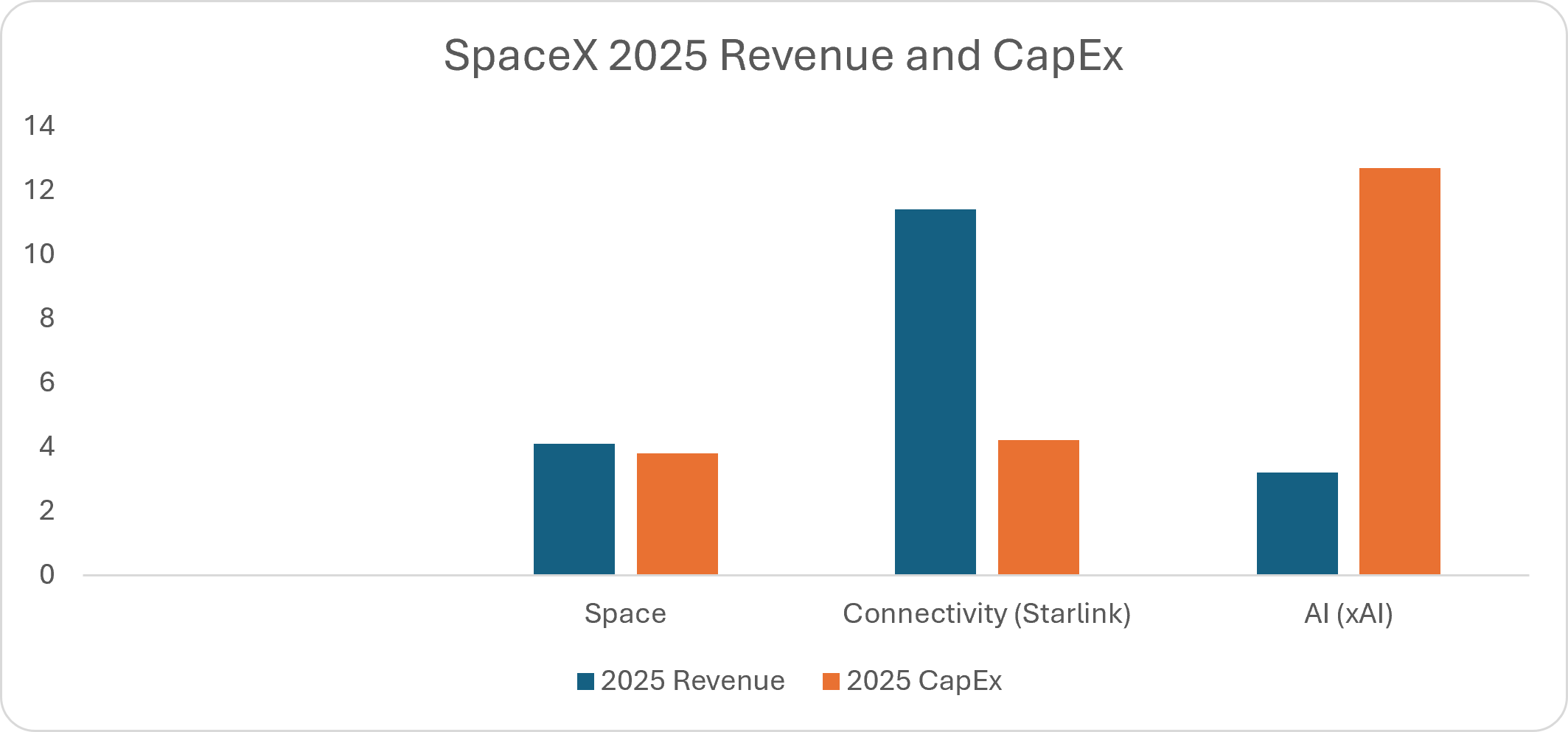

While SpaceX is perhaps best known either for its plans to colonise Mars or for its reusable rocket technology for ferrying people there, these are not major components of the future revenue projections with which SpaceX lured investors:

SpaceX has a profitable satellite business (Starlink), a small gimmick (space exploration) and a huge question mark (data centres in the sky). Maybe Starlink might have a value in the range of $250-500 billion but that places well over $1 trillion dollars responsibility on the AI business. The problem is that the technology for xAI’s most ambitious plans doesn’t yet exist. It might never exist in a viable commercial form. Even if it does come to exist, there’s no guarantee that xAI will extract over $ 1 trillion in net corporate value from it.

A century ago, the leap forwards to safety matches must have seemed at the time like adding AI to the internet seems to today’s consumers. Whoever owned global match supply would seemingly wield great financial power and influence. We know how that story ended.

Three hundred years ago, a master swindler reportedly secured deposits from investors for investment into “an undertaking of great advantage, but nobody to know what it is” and then fled the country.

Today the 4th largest traded company on the planet promises returns in investor capital based on technology that doesn’t even exist yet.

We worry that SpaceX could be the hare-brained heir of these schemes.

Paul Gambles is licensed by the SEC as both a Securities Fundamental Investment Analyst and an Investment Planner.

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit; it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledged all risks and have been informed that the return may be more or less than the initial sum