According to which version of the family history you believe, Panos Papademetriou reportedly changed his name either because he was trying to find work in a New York restaurant and encountered prejudice against hiring Greek waiters or because he fell in love with a French girl and wanted his name to sound French. Either way, his adopted, Franco-American name enabled him to find work in stockbroking, as did his son Theodore, known as Ted, both of whom worked at Shearson, Hammill & Co. Ted had risen to become a senior figure at Shearson when it merged with the fast-rising Hayden Stone, led by the star Wall Street figure of the 1960s, 1970s and 1980s, Sanford (Sandy) Weill. Ted worked closely with Sandy, and this relationship was a major factor in Ted’s son James (Jamie) choosing to work alongside Weill, despite more lucrative offers from the likes of Lehman Brothers.(1) A series of mergers and acquisitions ultimately led to Weill becoming CEO and Chairman of Citigroup in 1998. By this time, Jamie Dimon had spent 15 years working closely with Weill. Accounts differ as to the cause of the falling out between Dimon & Weill (2) but just over 6 months after the merger that left Weill running Citigroup, Dimon left and within a couple of years resurfaced as CEO of Bank One. Following JP Morgan Chase’s acquisition of Bank One, Dimon became CEO of JPM.

Dimon was later to gain kudos for steering JPM through the Global Financial Crisis of 2007-9 and its aftermath.

Credit Suisse was formed by Swiss politician and businessman Alfred Escher in 1856 and rapidly achieved prominence in Switzerland and beyond. In the 1980s and 1990s Credit Suisse embarked on a major programme of global expansion and by 2006 had overtaken long-standing rival UBS as the number one global private bank. Senior management do not appear to have considered or at least taken action to mitigate the conflicting paths of continuing to provide traditional Swiss banking privacy and secrecy on a global scale, while aiming to achieve substantial presence in America, where national political aims frequently clashed with much of Credit Suisse’s client base.

In 2009, Credit Suisse was subjected to a $536 million settlement following an investigation by the US and Manhattan Attorneys General into the bank’s secrecy arrangements with Iran and other US adversaries in the period from 1995 to 2006. In 2012, Credit Suisse and senior employees were fined for mismarking the prices of securities in 2007. Following the GFC a series of scandals and a raft of litigation has pursued Credit Suisse. Among others, these include being fined by ECB for participating as a member of a cartel engaged in exchange rate manipulation, a $2.6bn settlement with the Department of Justice for facilitating US tax fraud, fines by the Singaporean authorities for involvement in Malaysia’s 1MDB scandal, fines by US, UK and European regulators for enabling the then Mozambican finance minister to profit between 2012-26 from IMF loans intended to develop the country’s tuna fishing industry, further US DoJ fines for Foreign Corrupt Practices Act violations, being branded ‘discredit Suisse’ for legal fights with climate change activists (3), admitting engaging in espionage on the bank’s own employees, a number of suicides, a Bulgarian drug-trafficking scandal and involvement with the financial scandals surrounding Greensill Capital and Archegos Capital. (4)

Much of this persistent misconduct stems, in our view, from the group’s lack of transparency and lack of impartiality acting as both the generator and promoter of its own investment products thereby creating an overwhelming conflict of interest.

How has all this worked out?

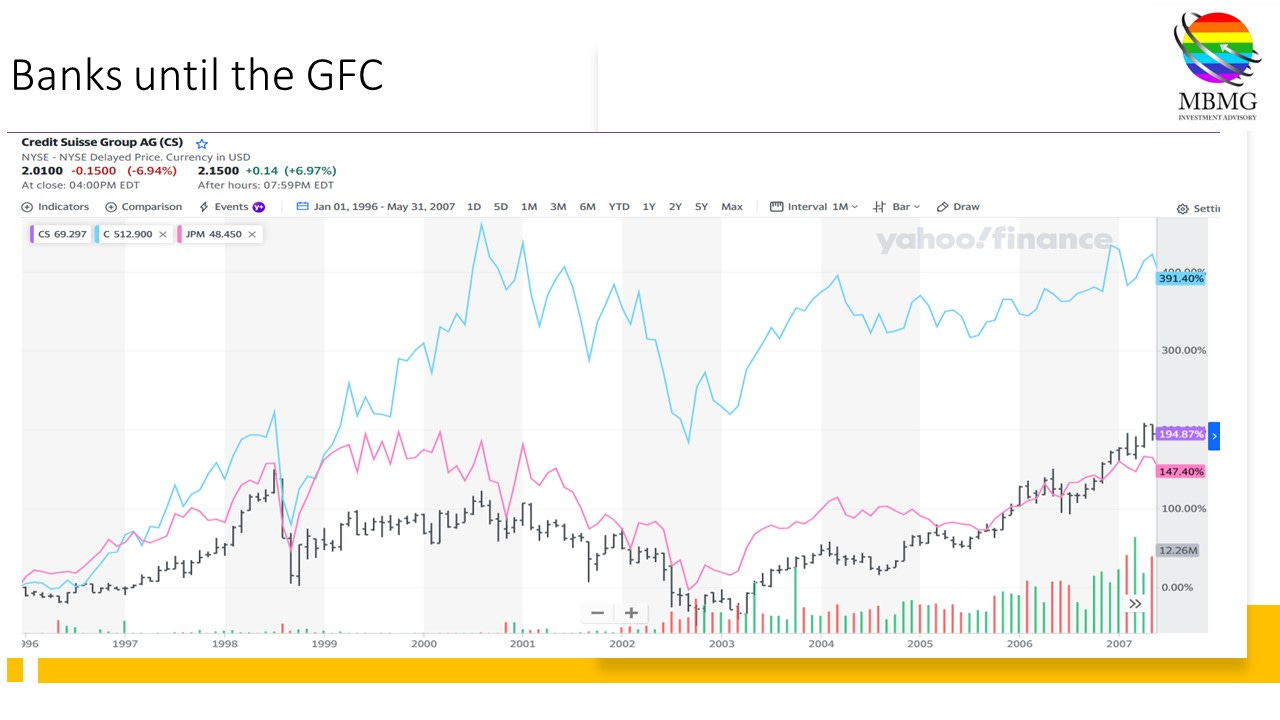

Well, in the period from Weill taking over at Citi until the GFC, Citigroup seemed to be the horse for investors, or perhaps punters, to back, increasing in value by 400% in less than 10 years (although that was all achieved prior to 2000-2002 crash). Credit Suisse shares increased almost 200% whereas JPM lagged, despite a high correlation to Credit Suisse, with a gain of ‘only’ around 150%.

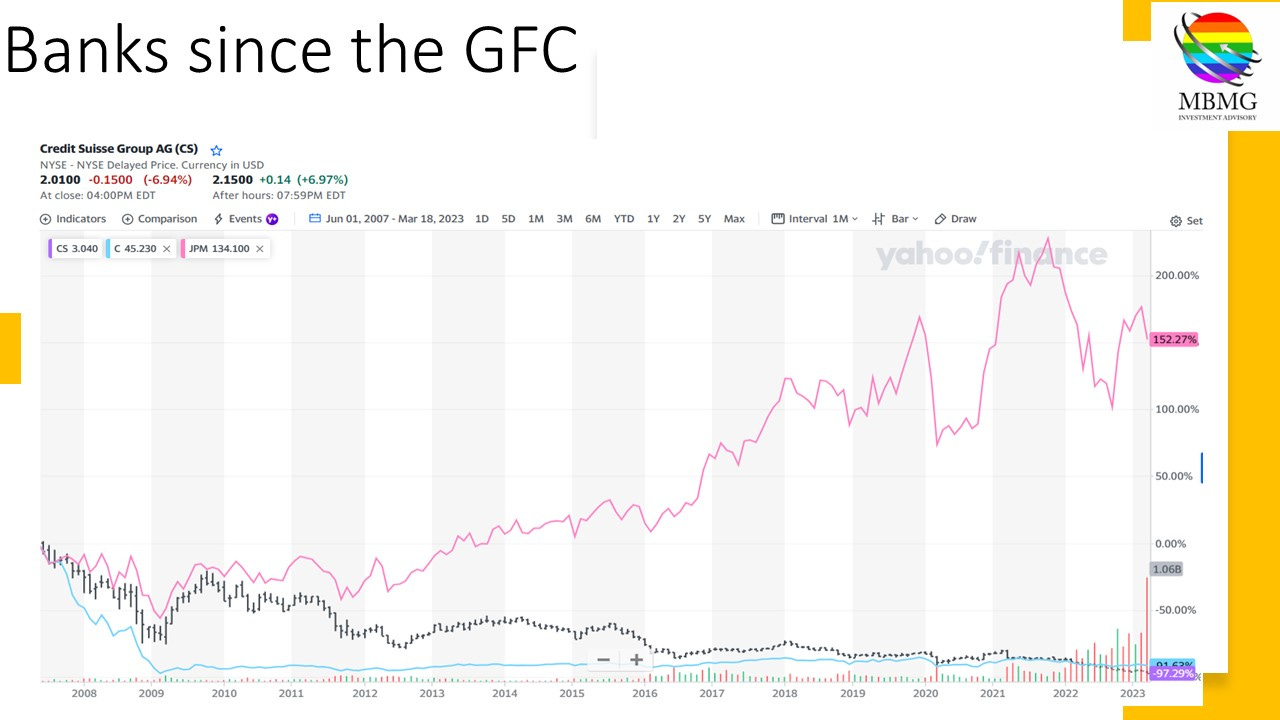

Since then however, the story has been different:

JPM, like Credit Suisse, recovered the losses of 2007-9 within less than 2 years. However, at this point, their fates diverged. JPM is currently at over 250% of its pre-GFC price, whereas Citi has fallen by over -90% from that time and Credit Suisse by over -97%!

The last 25 years has been a rewarding period for JPM investors, who have just about trebled their investment . Conversely, Citi investors have just over 20% of their original stake emaining and Credit Suisse investors have less than 5%

Since the beginning of last week (6th March) JPM stock has fallen by over -12%, Citi by over -15% and Credit Suisse by over -33%. JPM and Citi closed yesterday marginally above the lows of the day and the lowest close of the recent episode, whereas Credit Suisse had briefly spiked to over -40% down in intraday trading on Wednesday.

We have been asked whether these levels represent an attractive investment entry point. Our answer is “no - they may be an attractive speculation entry point but that is a different question.”

It is impossible to know how the cross currents in which banks are currently caught will play out. As in 2009, there will be big winners and there will be big losers. It may well be that Panos Papademetriou’s grandson continues to steer his company through the maelstrom better than the other leaders but at 67 years of age, it is unclear that Dimon will still be leading JPM in 25 years’ time.(5) It may be that JPM’s share price currently reflects a premium related to Dimon’s stewardship but this is just one added uncertainty in the most highly leverage and opaque sectors of the capital market.

Caveat investor but potentially great opportunity for speculators (to make or lose money)!

(1) Lehman presumably being flush with cash, having sold its broking division, Lehman Brothers Kuhn Loeb to Weill’s American Express Group, where it was merged with Shearson Hammill.

(2) The most popular theories posited involve either a power struggle between Dimon & Weill or Dimon’s refusal to promote Weill’s daughter, despite nepotism often seeming to be a founding principle of Wall Street.

(3) This incident led to Roger Federer terminating the arrangement by which Credit Suisse had been one of his core sponsors.

(4) See https://mbmg-group.com/article/liquid-lunge-seen-this-movie-before and https://mbmg-group.com/article/double-fault-unforced-errors-over-the-line-and-backhanders

(5) Dimon has faced increasing questions about his own retirement and has responded “My statement stays the same, it’s always five years. When and if we ever set an actual retirement date, we’ll let you know.” He has also stated a willingness to remain as President of the bank after his retirement.

This article relies on over 50 external and internal sources, references and resources. As always, a full bibliography is available on request but is not printed here in order to preserve space (the article is plenty long enough on its own!)

MBMG Investment Advisory is licensed by the Securities and Exchange Commission of Thailand as an Investment Advisor under licence number Dor 06-0055-21.

For more information and to speak with our advisor, please contact us at info@mbmg-investment.com or call on +66 2 665 2534.

About the Author:

Paul Gambles is licensed by the SEC as both a Securities Fundamental Investment Analyst and an Investment Planner.

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit, it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledged all risks and have been informed that the return may be more or less than the initial sum.