The Dangers of Sustaining Unsustainability

Human life is governed by complex systems - large complex systems that have evolved from smaller complex systems that in turn ultimately have their roots in much more straightforward individual action

Also available in presentation format https://mbmg.substack.com/p/sustaining-unsustainability or click the image below

Human life is governed by complex systems - large complex systems that have evolved from smaller complex systems that in turn ultimately have their roots in much more straightforward individual actions or particular responses to given events, challenges or situations.

This creates multi-layered interdependent complexities that shape the actions that we take - often these might involve unintended consequences, but they all reflect the priorities, interests and self-interests of those by or on behalf of whom the decisions were taken.

This is the ultimate invisible hand, which, rather than any conspiracy theory or powerful individual or group dictates actions, policies and decisions in all spheres of human life

The economy, the human brain and Earth’s ecosystem are all examples of complex systems whose components interact in non-linear ways, creating inherently unstable outcomes.

Think of the nursey rhyme of the old woman who swallowed a fly – we don’t know why she swallowed a fly and we know that it’s highly unlikely that she would have chosen to fatally swallow a horse to catch the fly but each step, from her internal (nursery rhyme) logic, in swallowing a spider, a bird, a cat, a dog, a goat, a cow and then a horse each to catch the other made sense…until finally, “she’s dead of course”.

Multiplying this complexity by almost 8 billion people sharing the same planet gives us a hugely complex system.

It's widely accepted now, based on mitochondrial DNA analysis that all of us here evolved from the same roots in Africa - what's also widely accepted but perhaps less widely known is that homo sapiens weren't the first hominins to venture out of Africa - Australopithecus, Homo habilis and Homo erectus also did so up to 2 million years earlier.

As did homo neanderthalis around 300,000 years ago.

Evidence suggests that homo sapiens started to leave Africa around 70,000 years ago and within 30,000 years had rendered extinct all the previous lineages of hominids - although they do live on in all of us - in that due to crossbreeding prior to the extinction, there is today a little bit of caveman and cavewoman in all of us - anyone of European ancestry is likely to be a few per cent neanderthal - so if you want to upset any white supremacists as much as I do, then if you meet any, you might mention to them that not only is their family line indigenously African, but in fact not only are they not ‘pure Aryan’, they're not even pure human.

Money existed from the earliest civilisations - People like Prof Niall Ferguson have tried to popularise a myth that earliest civilisations used barter but in fact the evidence indicates that they used money, accounting (in the forms of tally sticks or tablets - stone not ipad) and that as societies grew in size, this became an important basis of social organisation and control - in the ancient world, many and in some cases most slaves were debt slaves, debtors and/or their family members taken as security for non-payment.

The centralisation of this and the power associated with it seems to have played a large factor in the earliest development of the state from 5000 years ago.

The state used obligation and debt, and debt cancellation to enforce the will of the leaders (whether unitary, an oligopoly or in Ancient Greece and later in Aztec Mexico, a form of popular rule).

Debt cancellation was so successful in helping to maintain social order, that regular jubilees became a cause for celebration and feast day - today we continue to celebrate the longevity of rulers through jubilees, although we don't get the same benefits, of having our debts cancelled, that our predecessors did in more civilized times.

The aggregation of private wealth changed this dynamic so that over time instead of the state controlling debts and obligations and being the monopoly or dominant creditor, it began to compete against private lenders and ultimately had to borrow from them - to the extent that Herodotus wrote of Pharaoh Khufu's daughter having to work in a brothel to raise funding necessary for her father's ambitious pyramid project at Giza, although, like many morality tales involving debt this may be apocryphal.

Among early institutions to use the power of its acquired wealth to control the masses were religions - to the extent that the Christian church used debt forgiveness as one of its recruiting sweeteners for crusaders pressed into service against Islamic states in the religious wars that took place around 1000 years ago.

Conflict between states had always resulted in financial and economic rewards for victors inflicted on losers.

Among other tributes, Genghis Khan reportedly claimed that

"The greatest joy for a man is to defeat his enemies, to drive them before him, to take from them all they possess, to see those they love in tears, to ride their horses, and to hold their wives and daughters in his arms."

This helps to explain why he had over 500 concubines and why 1 in 8 men in Asia are descended from ’The Great Khan’.

The rewards led to greater competition between nations, which resulted in further borrowing by states - by the 14th century the great Venetian banking families had become of far greater financial significance than prototypical states like England which borrowed from them (and subsequently defaulted). By the 17th century, states, the corporate sector and the financial sector had evolved to a more recognisable form, just in time for the great geopolitical competition of the age of discovery

But ‘debtor states’ have always had a different relationship with so-called lenders, because state ‘borrowing’ has always been very distinct from individual or private borrowing.

State defaults to the private sector have never carried the same practical consequences as individual defaults - when Edward I defaulted in the 13th century, he simply changed the laws to banish from the kingdom the Jewish lenders from whom he'd borrowed (unless they forgave the debts and converted to Christianity).

From this crude exercise of state power, more nuanced distinctions evolved.

Also, the state exercises powers over all its citizens. Using this power in the nineteenth century, the British government introduced a temporary levy for one year to fund the cost of the Napoleonic Wars - it renewed this the following year and continues to renew it every year since - it's called income tax.

This encouraged state to flex its power as issuer of currency - in theory there were limits on this but as we discovered when the gold standard was suspended during World War One, was abolished during the Great Depression when privately owned gold confiscated by the US government and when it was vestigially consigned to history by Richard Nixon closing the gold window in 1971, these constraints were only arbitrary

This has been noted by empirical economists today who have started to formulate the actual role of government in modern economies.

We tend to label this 'fiscal policy' - the management or mismanagement by governments of surpluses or deficits.

Deficits- which are often mis-termed as increases in government debts (the accounting term 'debits would be more accurate' - are simply the government spending money into the economy.

Therefore, there are two ways in the modern economic system to create ‘money’:

- one is by government spending (which since 2008 has increasingly taken the form of government investment into capital market assets and has grown significantly in relative scale and importance)

- the other is by governments enabling or empowering commercial banks to do so by issuing loans (which represented by far the dominant form of money creation in the last decades of the 20th century)

As stated, policymakers globally since the GFC have, to a greater or lesser degree, directed flows to capital markets and therefore ultimately to asset prices - this has bolstered these and rehabilitated the global financial sector which is still, in varying degrees, existentially dependent on aggregate asset prices remaining inflated.

Sporadically since then policymakers have tried to pull back from this but failed because each time they've done so, it's highlighted the dependence of the global financial sector on maintaining these prices - the current episode of monetary tightening and financial asset disposals (although so far, these have been minimal) is the most serious attempt yet. This year, we've all seen the early consequences of this and we're already seeing rumblings, whether UK pensions or European mega-banks, of the fractures in the system that are being highlighted.

It seems highly likely that once again, having created a bit of 'space' to do so, policymakers will once again pivot back to cutting interest rates and to aggressively buying assets again - this will likely drive up asset prices and boost the financial sector but every time they do this, the consequences of making more room next time to fix it again in the future will simply get greater and greater, creating the risk that they will one day we run out of road, having created a problem that's just too big to fix.

We appear to be still some way off that but the current bump in the road can get far bumpier before we're back to a smoother ride and the current bump will seem pancake flat compared to future episodes. One of the greatest 20th century economists, Hyman Minsky, termed processes such as this as futile and ultimately costly exercises in trying to stabilise instability - I don’t think that there are any indications that the system is likely to change in the short term so the best any of us can do is be aware that this isn't sustainable, that it will get more volatile, that there will be patches of smooth road in between and to plan accordingly

Of course there is another meaning to sustainable - a more important one than existential threats to financial markets - and that is existential threats to the planet.

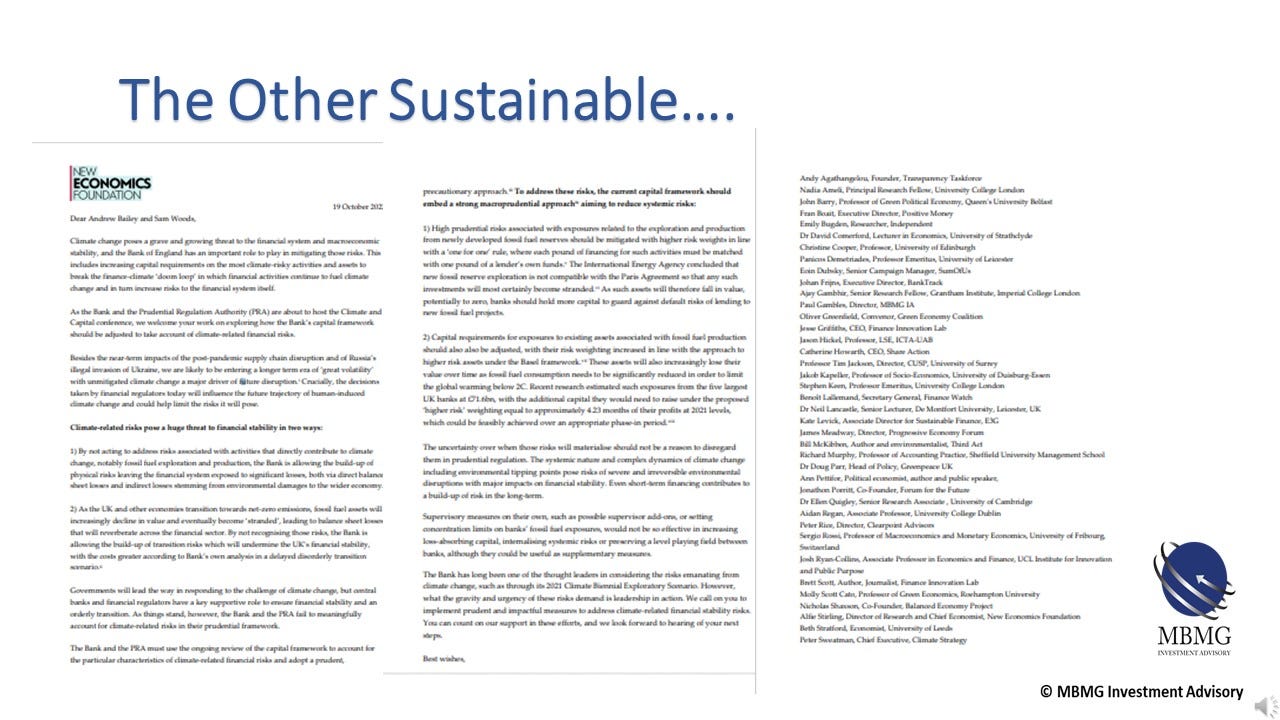

Resources represent the ultimate limit to growth and this is why I recently signed a letter to Andrew Bailey at the Bank of England - along with 40 or so much more eminent, much more important experts. (https://neweconomics.org/uploads/files/Open-letter-to-BoE_-climate-and-capital.pdf)

It's the second such letter I've been involved in sending Governor Bailey - he replied to the first one - he hasn't replied to this yet.

But even if he does reply, I'm doubtful that he will, as we all asked him to do, break the climate-finance doom loop. In fact, that doom loop seems to be self-reinforcing.

Over twenty years ago, some well-intentioned people at the UN came with the Millennium Development Goals, which evolved into the Social Development goals, which in turn morphed into the basis for ESG (environmental social and governance - something that you're going to be hearing more and more and more and more about).

While this was also no doubt well-intended, in the same way that obligations between individual members of society resulted in a parasitical financial sector that has spawned an unsustainable socio-economic burden, attempts to conserve a habitable planet have resulted in a profit centre that is being exploited in a way that is ultimately detrimental to sustainability - it has become far easier and more financially rewarding to observe adherence to ESG criteria than to do anything meaningful about sustainability.

This too will continue seeming to work until it doesn't - previous hominins survived up to 2 million years until homo sapiens rendered them extinct - homo sapiens have been in existence for 70,000 years and represent the biggest known threat to their own existence

MBMG Investment Advisory is licensed by the Securities and Exchange Commission of Thailand as an Investment Advisor under licence number Dor 06-0055-21.

For more information and to speak with our advisor, please contact us at info@mbmg-investment.com or call on +66 2 665 2534.

About the Author:

Paul Gambles is licensed by the SEC as both a Securities Fundamental Investment Analyst and an Investment planner.

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit, it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledge all risks and have been informed that the return may be more or less than the initial sum.