Why you can't rely on the Fed (now more than ever)

Fight the Fed? I’d string ‘em up!!

“The monetary climate – primarily the trend in interest rates and Federal Reserve policy – is the dominant factor in determining the stockmarket’s major direction” [1]

The problem is that the Fed seems to lack any kind of consistent direction – it’s hard to know whether you’re actually fighting the Fed or simply anticipating their next 180 degree policy u-turn.

That said, there’s a very clear disconnect right now between policymaker ‘guidance’ and market sentiment. Markets have decided, in the face of extremely unconvincing Fed claims to the opposite, that tightening of monetary policy including the area of liquidity creation created by the Fed that seems to bridge both monetary and fiscal policy, is close to peaking and that the peak will be followed by a rapid softening.

This seems largely based on expectations that inflation, largely caused and exacerbated by policy mistakes has peaked (and therefore that policymistakes, or at least inflationary policy mistakes have peaked).

Whilst it’s certainly a plausible view and one that reflects our own base case on inflation, there are 3 main risks to that

i. While it seems highly unlikely that demand will drive inflation higher in broad structural terms. there are upside inflation risks (China re-opening, continued geopolitical policy aggression, leading to further conflict and sanctions and above all resource disruptions, not least due to exogenous factors such as climate).

ii. Even if inflation moderates, it’s far from clear that policymakers will moderate policy sufficiently quickly or aggressively – in fact, they’re telling us as clearly as they ever communicate anything that they won’t. Markets may be guilty of imposing a degree of rational expectation on policymakers that is simply unwarranted. In other words, if the Fed were a serial killer who had already murdered dozens of victims, each market participant is assuming that they’re safe because the Fed has no reason to harm them so it would be crazy for the Fed to do so. Relying on the criminally insane to behave in a measured and reasonable fashion, when they haven’t done so previously is a highly unreliable strategy.

iii. Even if inflation moderates and even if policymakers ‘pivot’ in response, there’s no guarantee that policymakers have the policy tools (or the competence using them) to achieve soft landings that have been so illusory in the past.

And yet, investors have to respond to these challenges in real time.

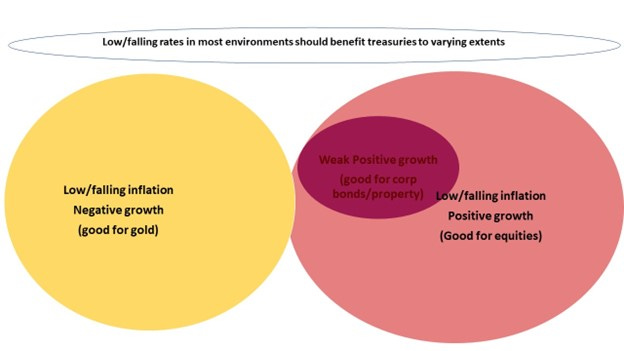

We would continue to weight primarily toward assets that are inversely correlated to interest rates but with varying degrees of correlation to growth:

– long treasuries will benefit from interest rate cuts irrespective of economic conditions

-gold is likely to benefit irrespective of conditions but particularly so in an economic downturn

-equities should benefit from rate cuts but ultimately only if earnings are supported – rate cuts and weaker earnings could lead to further equity weakness

Corporate bonds, especially lower credits, remain dependent on spreads remaining relatively tight, aligning them, like commercial property, more with equities – if equities require a Goldilocks scenario, then corporate bonds and property require that specific Goldilocks subset made up by the coolest quartile of the ‘not too hot, not too cold’ scenario. Therefore, in 2023, expectations of easier monetary policy are only one part of the capital market conundrum:

The combination of uncertainty about rates going forwards and beyond that about the earnings outlook not only heightens inter-asset volatility but also inter-regional volatility and exchange rate volatility – one key for investors from here will be currency exchange rates – Asia’s international investors largely benefitted from domestic currency weakness in terms of international asset values last year – this year could be the complete opposite (or not!)– Asian investors need to be aware of the heightened FX risks of holding foreign assets.

Don’t fight the Fed.

But don’t ignore them either.

Above all, don’t rely on them. The uncertainty facing us all in 2023 is largely a consequence of policy mistakes.

We shouldn’t assume that policy makers will suddenly acquire competence.

But we can’t rely on them to always get it wrong either.

[1] Winning on Wall Street by Marty Zweig, who purportedly summarised the same point by coining the phrase ‘Don’t fight the Fed!

Disclaimers:

1. While every effort has been made to ensure that the information contained herein is correct, MBMG Investment Advisory cannot be held responsible for any errors that may occur. The views of the contributors may not necessarily reflect the house view of MBMG Investment Advisory. Views and opinions expressed herein may change with market conditions and should not be used in isolation.

2. Please ensure you understand the nature of the products, return conditions and risks before making any investment decision.

3. An investment is not a deposit, it carries investment risk. Investors are encouraged to make an investment only when investing in such an asset corresponds with their own objectives and only after they have acknowledge all risks and have been informed that the return may be more or less than the initial sum.